Preview of the Week Ahead

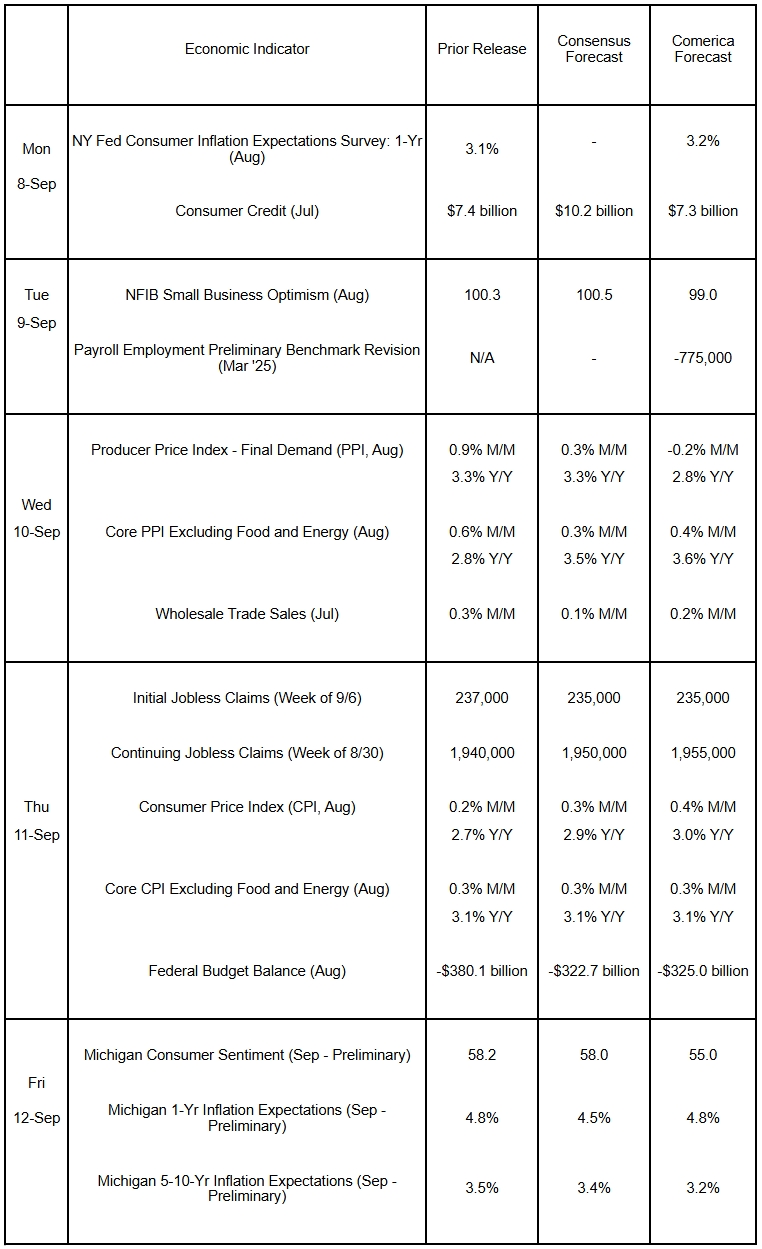

Payroll employment is forecast to be revised down by 775,000 in the Preliminary Benchmark Revision’s release on Tuesday. This release revises the level of employment in March 2025 using unemployment insurance records covering approximately 11,000,000 workplaces—considerably more detail than is available to the government’s statisticians when they publish the monthly jobs report, which is based on survey responses from about 50,000 workplaces. If the revision is as negative as forecast, it will show the economy had less momentum entering 2025 than previously believed. This would have less implications for monetary policy than the weaker-than-expected August jobs report published last week. Even so, a weak Benchmark Revision would add pressure for the Fed to cut at the next decision September 17.

CPI and PPI inflation will likely diverge again in their August releases as lower diesel prices hold down the year-over-year increase of the PPI. The core CPI and PPI indexes are forecast to run hot again and pick up in year-over-year terms on tariff passthrough. Shelter inflation will likely run cool in the CPI report, offsetting some of the inflationary pressure from tariffs.

The Week in Review

The job market weakened again in August. U.S. employers added a lean 22,000 nonfarm payroll jobs in the month, below the 75,000 consensus forecast or Comerica’s forecast of 45,000. Job growth in June and July was revised down a net 21,000. Following revisions, job growth in the last three months averaged a weak 29,000, worse than the 35,000 reported in the prior report (which is now revised down to 28,000). August saw employment fall in key goods-producing and service-providing industries. Employment fell across goods-producing industries, down 12,000 in manufacturing, 7,000 in construction, and 6,000 in mining and logging. In service-providing industries, there were declines of 17,000 in professional and business services and 12,000 in wholesale trade. Healthcare and social assistance added 47,000 jobs, leisure and hospitality added 28,000, and retail added 11,000. Tariffs and AI seem to be weighing on private job growth. Government jobs fell 16,000.

The unemployment rate rose to 4.3% from 4.2% and was the highest since October 2021. In the survey of households, the labor force increased 436,000, employment rose 288,000, and unemployment rose 148,000. The labor force participation rate edged back up to 62.3% from July’s 62.2% and matched June’s level. The employment-to-population ratio tied July for the lowest since December 2021, but the employment-population ratio for prime-age workers aged 25-54 edged up on the month to 80.7% from 80.4% in July. Average hourly earnings rose 0.3% on the month, matching expectations, and slowed to a 3.7% increase from a year earlier from 3.9% in July. August’s wage growth was the second-weakest since May 2020. The average workweek was 34.2 hours, with July revised down to match that level.

The ISM manufacturing PMI rose to 48.7 in August from 48.0 in July, while the services PMI rose to 52.0 from 50.1. The weak August jobs report and lukewarm PMIs reinforce expectations for the Fed to cut interest rates at the September meeting. Comerica forecasts quarter percentage point rate cuts at the Fed’s September, December, and March 2026 meetings.

For a PDF version of this publication, click here: Comerica Economic Weekly, September 8, 2025

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.