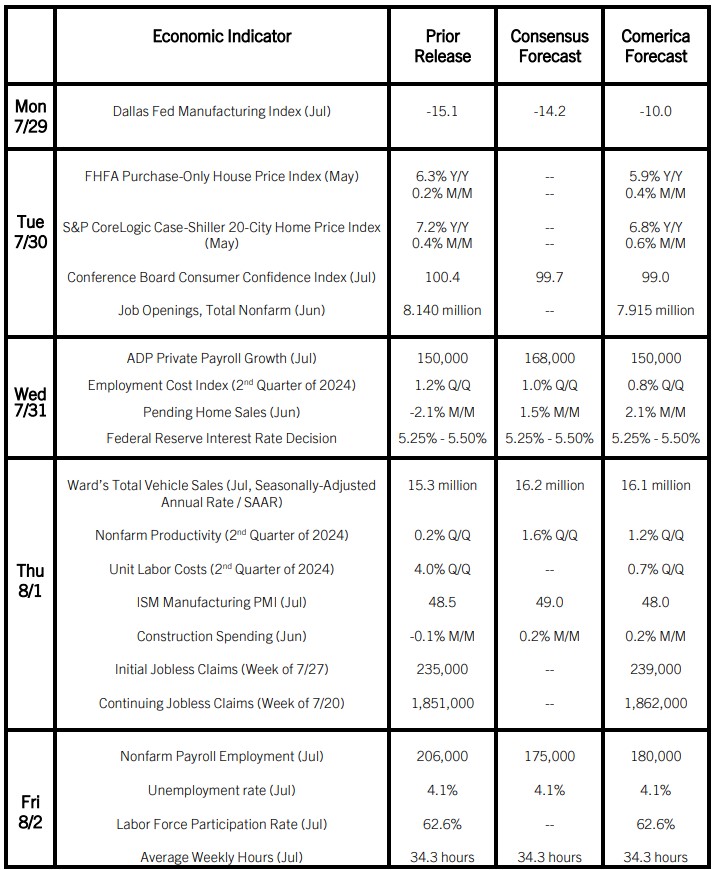

Preview of the Week Ahead

The Fed is expected to hold interest rates steady at their July 31 monetary policy decision, but signal to expect a rate cut at the next decision on September 18. Last week’s solid GDP report reassured the Fed that there is no urgency for an immediate rate cut.

Payrolls growth likely slowed a bit in July from June and registered slightly above the second quarter’s 177,000 monthly average increase. The unemployment rate is expected to hold steady near 4%, indicating a normal margin of slack has returned to the job market. Average hourly earnings likely grew modestly from June and registered the slowest year-over-year increase since 2021. The latest Job Openings and Labor Turnover Survey, released at a one-month lag to the jobs report, will likely show churn in the job market was minimal in June. Employers are cautious about hiring, but not making big layoffs either, and far fewer workers are quitting jobs for external opportunities than in 2021 or 2022.

House price indexes likely rose solidly on the month in May but moderated in year-over-year terms, mirroring the slower annual increases of median home sales prices in recent months. With more listings for homebuyers to choose from and headwinds to demand from high mortgage rates and prices, home price increases are likely to moderate further in the rest of 2024.

The Week in Review

The economy grew by 2.8% annualized in the second quarter according to the advance estimate, well above the 1.9% consensus forecast. Consumer spending rose by 2.3% annualized, with increased spending on both goods and services. Nonresidential fixed investment rose by a solid 3.6% annualized. Government spending expanded at a robust pace as well. Inventory accumulation added about a percentage point to the quarter’s annualized growth. The trade deficit was a headwind as imports rose faster than exports, and lower sales of new and existing homes weighed on residential investment.

The GDP Price Index, up 2.3% annualized, slowed from the first quarter’s 3.1% increase. Inflation by the Personal Consumption Expenditures Price Index (PCE Inflation), the Fed’s preferred inflation metric, also slowed, to 2.6% annualized from 3.4% in the first quarter. Monthly data show PCE inflation slowed to 2.5% in year-over-year terms in June from 2.6% in May and was the lowest in more than three years.

Sales of existing homes tumbled by 5.4% in June to an annualized rate of 3.89 million units. The median home price rose 4.1% from a year earlier to a record $426,900, but its rate of increase was the slowest since last December. Existing home listings rose again. With listings up and sales down, listings were equivalent to 4.1 months of supply, the highest in four years. New home sales eased by 0.6% in June to an annualized rate of 617,000 units and were down notably from a year earlier. The $417,300 median sale price of a new home was essentially unchanged from a year earlier.

For a PDF version of this publication, click here: Comerica Economic Weekly, July 29, 2024

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.