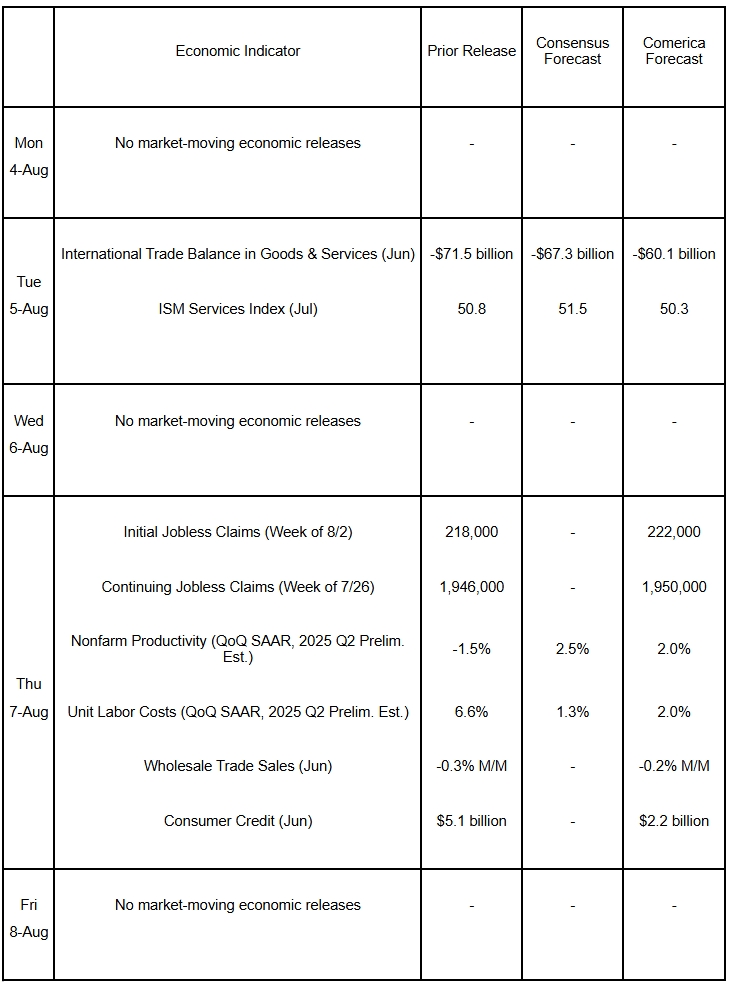

Preview of the Week Ahead

The economic calendar is light this week. The trade deficit is expected to have fallen sharply in June as goods imports declined further on the back of steep tariffs increases. The ISM Services PMI will probably show the services sector expanded for the second consecutive month, albeit at a slower pace. Productivity likely rebounded to growth in the second quarter, and unit labor cost increases slowed. Consumer credit likely rose at a modest pace for the second successive month in June.

The Week in Review

President Trump imposed new tariff rates on imports from most U.S. trading partners on August 1st, ranging from 10% to 50%. Imports from two of America’s largest trade partners—Canada and China—will be levied hefty tariffs of 35% and 30%, respectively (Canadian goods that are tariff-free under USMCA stay exempt). Tariffs on imports from Mexico, another major partner, will remain at 25% after bilateral negotiations were extended another 90 days. Goods imports from Mexico, China, and Canada totaled $1,375 billion in 2024, two-fifths of all U.S. goods imports. The U.S. is imposing a 15% tariff on most goods imported from the EU; the EU also pledges to buy $750 billion of U.S. energy products and invest $600 billion in the U.S. The European Union is America’s largest trading partner, with two-way trade of nearly $1.5 trillion in 2024. The U.S. ran a nearly $240 billion trade deficit in goods with the EU last year. The Yale Budget Lab estimates that after the August 1 increases, the average U.S. tariff rate is up about 15 percentage points this year, a tax hike of about 1.5% of GDP.

As expected, the FOMC held the federal funds target steady at a range of 4.25% to 4.50% at their July 30 decision. Two FOMC members dissented, favoring a 0.25% cut. But neither the FOMC’s policy statement nor Chair Powell’s comments at the press conference signaled a rate cut imminent at the next decision on September 17th. Real GDP expanded by 3.0% annualized in the second quarter, stronger than expected. Reversing the first quarter’s surge, imports cratered in the second quarter. The decline in imports made a very large contribution to growth. Most other components of GDP were soft in the second quarter. Consumer spending rose by a moderate 1.4% annualized. Business investment and government spending rose modestly, while residential investment fell. Exports also declined. The GDP Price Index and the Personal Consumption Expenditures Price Index rose around 2.0% annualized. In the first half of the year, real GDP averaged a 1.2% annualized increase, down from 2.8% annual growth in 2024.

The July jobs report was weaker than expected. 73,000 jobs were added from June, near Comerica’s 80,000 forecast but below the 104,000 consensus. Job growth in the prior two months was slashed a big 258,000. After revisions, job growth averaged an anemic 35,000 in the last three months, down sharply from the 150,000 three-month average in the prior report. The unemployment rate edged up to 4.2%, matching its second quarter average. The labor force participation rate fell to 62.2%, the lowest since November 2022. The average workweek rebounded slightly to 34.3 hours. Wages rose by 0.3% in July and were up 3.9% from a year ago, faster than June’s 3.8% increase. After the weak jobs report’s release, President Trump instructed his administration to fire the Commissioner of the Bureau of Labor Statistics, who served in both Republican and Democratic administrations over the last 20-plus years.

For a PDF version of this publication, click here: Comerica Economic Weekly, August 4, 2025

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.