Fed forecast to cut again at October and December meetings;

Economy may hit an air pocket in the 4th quarter, but should regain traction in 2026

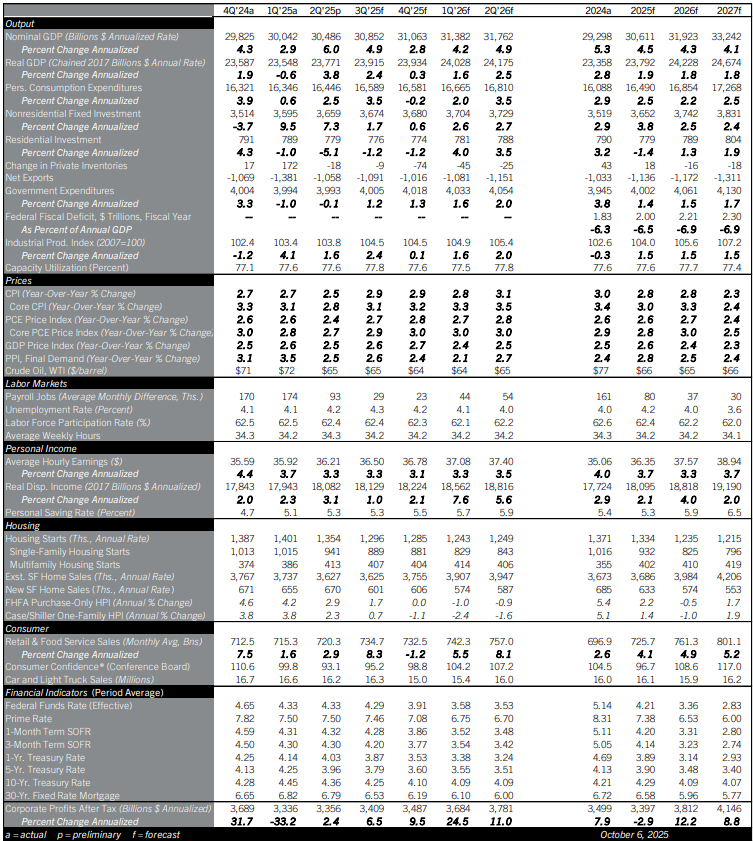

The Fed finally pivoted to rate cuts in September after a raft of weak jobs releases and downward revisions downgraded their view of the labor market. The August jobs report was considerably weaker than expected, with anemic payrolls growth, downward revisions to prior months, and the unemployment rate edging up to the highest since late 2021. The Preliminary Benchmark Revision released September 9 made further downward revisions to payrolls, and confirmed a weak trend of job growth throughout this year. Following these releases, the Fed cut the federal funds target a quarter percent on September 17. Jobs data since then have continued to disappoint. Payroll processing company ADP reported a 32,000 decline in private employment in September, likely the clearest read on job growth while the federal shutdown delays the BLS’ jobs report. Comerica forecasts for the Fed to cut their target rate a quarter percent at both their late October and mid-December decisions, to a range of 3.50% to 3.75% by year-end. The Fed is also forecast to end run-off of their bond holdings (“Quantitative Tightening”) in early 2026.

Real GDP has been volatile in 2025, with a modest contraction in the first quarter followed by catchup growth in the second; Comerica forecasts a solid third quarter, as well. Some of this mid-year strength is payback after volatility of imports and inventories fueled the first quarter’s drop. Also, consumer spending picked up in the second and third quarters as Americans cashed in on EV subsidies before they lapsed on September 30.

Real GDP is forecast to hit another air pocket in the fourth quarter. Auto sales will take a step back without the subsidies. The federal government shutdown that began October first will be a headwind, too; in prior shutdowns, each week of shutdown shaved 0.1 to 0.2 percentage points from annualized real GDP growth in that quarter, with about half of the foregone growth recovered once the government reopens. Tariff-fueled inflation is another nagging headache for the private sector, squeezing margins, pressuring businesses to slow-roll hiring and investment, and eating into consumers’ purchasing power.

Even so, there are even more important tailwinds that will likely help the economy regain traction in 2026. Not only is the Fed cutting rates, fiscal policy will turn expansionary as the July 4 fiscal bill raises spending on defense and immigration enforcement and cuts corporate and individual taxes. Even more importantly, AI is fueling a boom in investment in software, computing equipment, data centers, and electricity generation; the long gestation periods for these projects mean they should continue to propel the economy into 2026 at least. Finally, existing home sales should begin to recover next year as mortgage rates fall and start to unbottle long-pent-up demand, albeit at prices that are a bit lower than the peaks reached in early 2025.

For a PDF version of this publication, click here: October 2025 U.S. Economic Outlook

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.