Preview of the Week Ahead

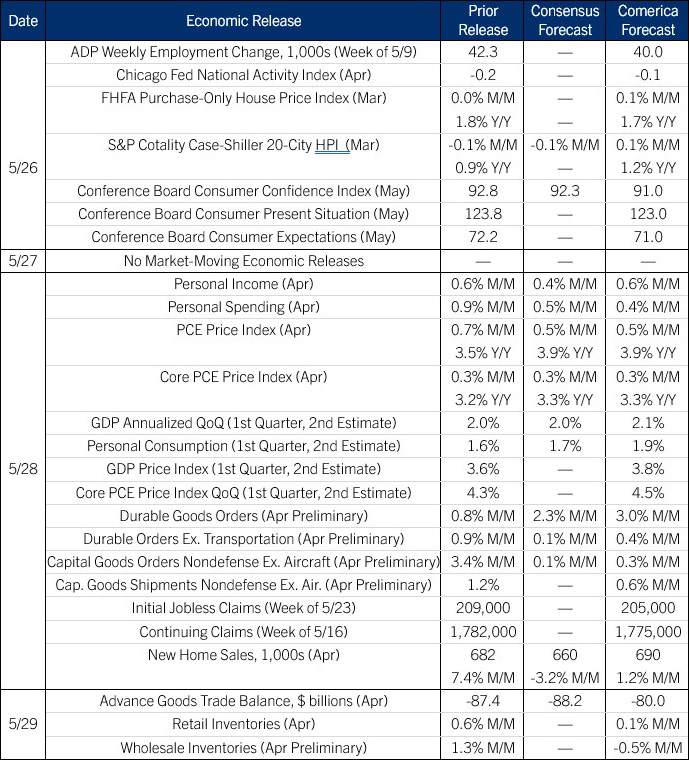

Inflation as measured by the PCE price index likely rose to around 4% in April as gas prices climbed; the PCE is the Fed’s preferred inflation gauge. April likely delivered more solid gains in personal income and spending, but those gains were largely swallowed by inflation. The core PCE price index was likely little changed, hovering around three and a quarter percent. The Fed has made clear they are unhappy to see it stuck above their 2% target.

Real GDP growth for the first quarter is likely to be revised higher in the second estimate, reflecting upward revisions to consumer spending. Inflation in the first quarter also is likely to be revised higher.

The Conference Board’s Consumer Confidence Index© likely edged lower in May as gas prices reached new four-year highs. Even so, this measure of sentiment should still look considerably better than the University of Michigan’s Consumer Sentiment Index, which is at a record low. The Conference Board’s Index remains only slightly below its post-2000 average.

Durable goods orders likely registered another solid increase in April as more civilian aircraft orders came in. Core orders excluding aircraft and other volatile categories likely rose as well, though at a more moderate pace. Manufacturing has picked up since the turn of the year.

The Week in Review

Minutes from the Federal Open Market Committee’s April meeting showed that “a majority” of FOMC members see a rate hike as a possibility “if inflation were to continue to run persistently above 2 percent.” While the committee left the forward guidance in their April statement unchanged—with a mild lean toward easing—“many” FOMC members would have preferred to strip that bias out. The FOMC isn’t sending a strong signal in either direction; uncertainty is everywhere in the minutes (mentioned 11 times). Practically speaking, the Fed is unlikely to raise rates unless tariff- and energy-driven inflation begins to seep into more domestically determined prices: labor-intensive services or housing costs, for example. That still seems unlikely given modest job growth and a clear margin of slack in the labor market.

Housing data perked up last week. The NAHB/Wells Fargo Housing Market Index rose to 37 in May from 34 in April, returning to pre-war levels. Current sales conditions, sales expectations, and homebuyer foot traffic all improved. The National Association of Realtors’ Pending Home Sales Index rose 1.4% in April, registered its strongest April reading since 2023. The index tracks contract signings and is a strong leading indicator of existing home sales.

The U.S. 10-year Treasury yield rose to near 4.7% last week, its highest since early 2025, as oil prices rose. Crude oil futures and the 10-year yield often move in tandem. U.S. crude oil inventories fell by the largest amount on record last week as exports jumped. Domestic crude oil production also rose sharply in the first two weeks of May but remains below December’s level.

For a PDF version of this publication, click here: Comerica Economic Weekly, May 25, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.