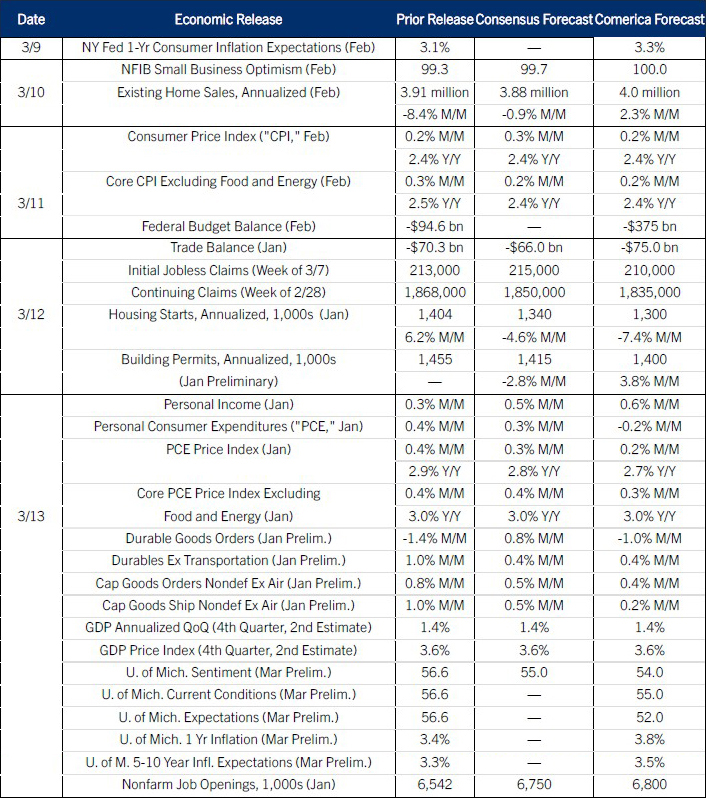

Preview of the Week Ahead

The February CPI report will likely run cool as tame housing costs offset the effects of tariffs. Grocery price inflation was likely tame during the month. The January PCE inflation report likely ran hotter, since medical services make up a larger share of the PCE price basket, and those prices tend to jump at the start of the year. The federal deficit likely widened sharply in February as the 2025 tax cuts reduce income tax receipts.

These inflation reports cover the period before the war with Iran, so they do not reflect its effects. But the preliminary March release of the University of Michigan’s consumer survey will: Sentiment likely retreated from February as the headlines and rising gas prices pushed inflation expectations higher.

The Week in Review

The outbreak of war with Iran and a weak February jobs report are clouding the U.S. economic outlook. U.S. crude oil futures jumped to their highest level since 2023 in the first week of the conflict, driving gasoline prices up more than 30 cents per gallon and diesel up more than 50 cents per gallon since the start of the month. The U.S. has been a net exporter of petroleum products since 2019, which mutes the shock to domestic energy prices; energy prices are spiking even higher in Europe, a net petroleum importer.

The February jobs report was much weaker than expected, with payroll job losses, a higher unemployment rate, and big downward revisions. Employers cut 92,000 payroll jobs, the second-worst month after DOGE layoffs reduced federal payrolls by 166,000 in October 2025. Accommodation and food services cut 35,000 jobs, likely partly due to severe winter weather disrupting hourly work. Healthcare fell 28,000 because of a big strike falling in the survey week. Those temporary factors don’t explain losses across many other industries, including manufacturing, construction, private education, administrative and support services, and couriers and messengers. The unemployment rate rose to 4.4% from 4.3% as the labor force participation rate fell to 62.0% and reached the lowest level since late 2021. Most of its decline reflects workers retiring as the population ages; the participation rate for workers aged 25-54 edged down but was still near the highest since 2001.

The February release included big revisions to the household survey in its annual benchmarking. The benchmark revised down employment in December 2025 by 1.43 million, reduced the labor force by 1.42 million, and raised unemployment a much smaller 15,000. Incorporating these revisions, employment fell 35,500 per month in the 12 months through February, 2026.

The Fed will worry about this weak report, but other data suggest it overstates February’s weakness. The ISM Services PMI jumped to the strongest since 2022 in February, while the ISM Manufacturing PMI posted its two best readings since then in January and February. The Fed began the year expecting tailwinds from interest rate cuts, tax cuts, and higher government spending. The February jobs report will make them reassess that outlook, but doesn’t provide enough evidence to re-write it. That makes an interest rate cut very unlikely at the Fed’s mid-March decision, especially since rising energy prices will push inflation higher near-term.

For a PDF version of this publication, click here: Comerica Economic Weekly, March 9, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.