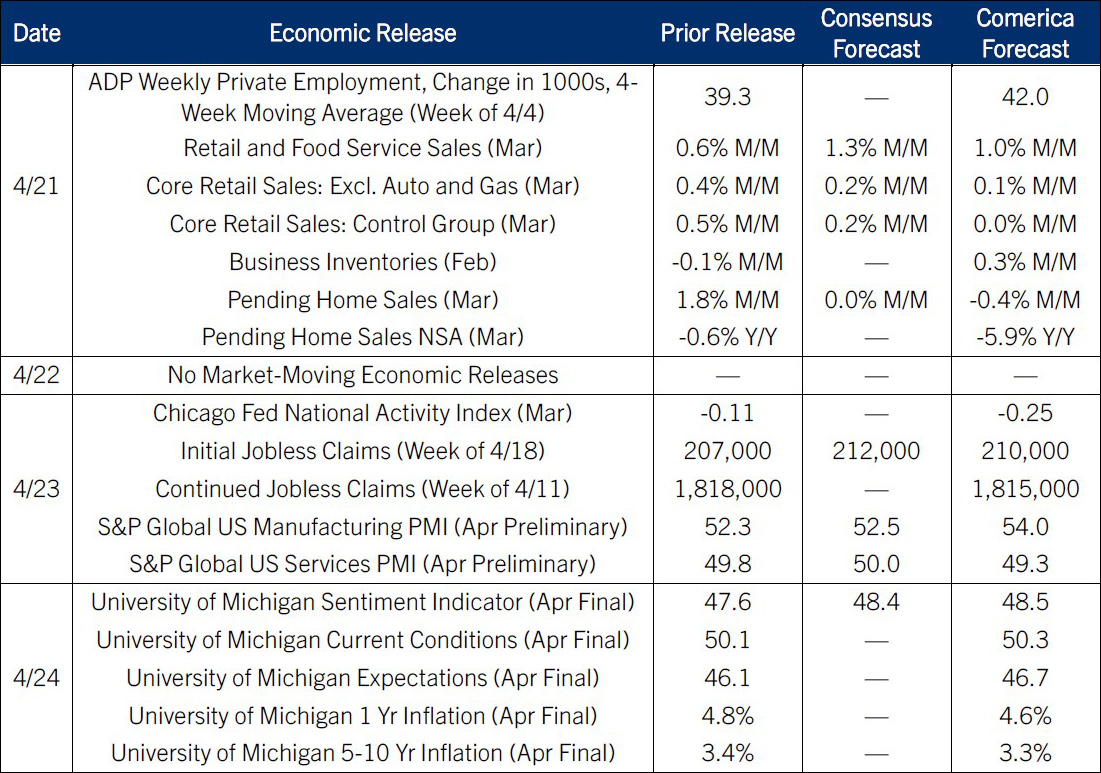

Preview of the Week Ahead

Retail sales jumped in March as consumers paid more to fill gas tanks, but sales excluding gasoline stations were likely about flat. Pending home sales likely fell as the war and higher mortgage rates gave some homebuyers cold feet. On the bright side, the University of Michigan’s Consumer Sentiment Indicator will likely be revised up from the preliminary release, which fell to a record low. Survey responses collected since the ceasefire will likely be stronger, as lower oil prices and calmer financial markets allay consumers’ worries. ADP’s weekly private payrolls report will likely deliver another encouraging signal. This relatively new statistic doesn’t move financial markets as much as the monthly jobs reports published by the government and ADP, but it is likely a useful leading indicator for them. This release will likely show job growth rose above 40,000 per week, equivalent to more than 160,000 per month. If borne out in the monthly data, that would be the fastest private payrolls growth since late 2024.

The Week in Review

Oil futures prices pulled back last Friday to the lowest levels since early March as Iran and the U.S. extended the ceasefire, and as shipping through the Strait looked likely to resume. Prices rebounded Sunday night, but were still lower than in the last three weeks. Producer prices rose 0.5% in March, a sizable undershoot of consensus expectations for a 1.1% increase. Higher prices of petroleum products were offset by lower prices for fresh fruits and vegetables and narrower wholesalers’ margins, both of which had risen sharply at the turn of the year. The PPI subindex for natural gas also fell after a surge in February—unlike oil, surging natural gas prices overseas have not passed through to domestic prices. Core PPI excluding foods and energy rose just 0.1% on the month.

The Federal Reserve’s Beige Book survey of contacts across the U.S. economy shows that the war has raised inflation and uncertainty through early April, but hasn’t derailed economic activity. Economic activity expanded “at a slight to moderate pace” in eight of 12 Reserve Districts, up from seven districts in the prior report. Housing activity softened as consumers turned more cautious, but commercial real estate markets improved on strong demand for data centers. Industrial production and existing home sales undershot expectations in March. Industrial production fell 0.5% on a 2.3% drop in utilities—warmer weather—and a 1.2% drop in mining. Manufacturing edged down 0.1%. Manufacturing output is up 0.5% from March 2025, the last month before Liberation Day, but output of auto products is down 5.6%. Employment in auto and parts manufacturing fell 22,500 or 2.3% over the same period, according to the March jobs report.

Existing home sales pulled back to a 3.98 million annual rate in March from 4.13 million in February, undershooting expectations. The median existing-home price rose 1.4% from a year earlier to $409,000. There were 4.1 months’ supply of homes listed for sale in March, consistent with a balanced market, albeit with supply and demand both weak. The National Association of Home Builders / Wells Fargo Housing Market Index fell in April to the lowest level since last September. The release matched Comerica / Fifth Third’s forecast, which was the most pessimistic among the 23 responses in Bloomberg’s survey. Homebuilders reported softer sales and foot traffic during the month and were more downbeat about the outlook. Similarly, the NFIB Small Business Optimism Index fell in March to the lowest level since Liberation Day, near our forecast and below the consensus.

For a PDF version of this publication, click here: Comerica Economic Weekly, April 20, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.