Preview of the Week Ahead

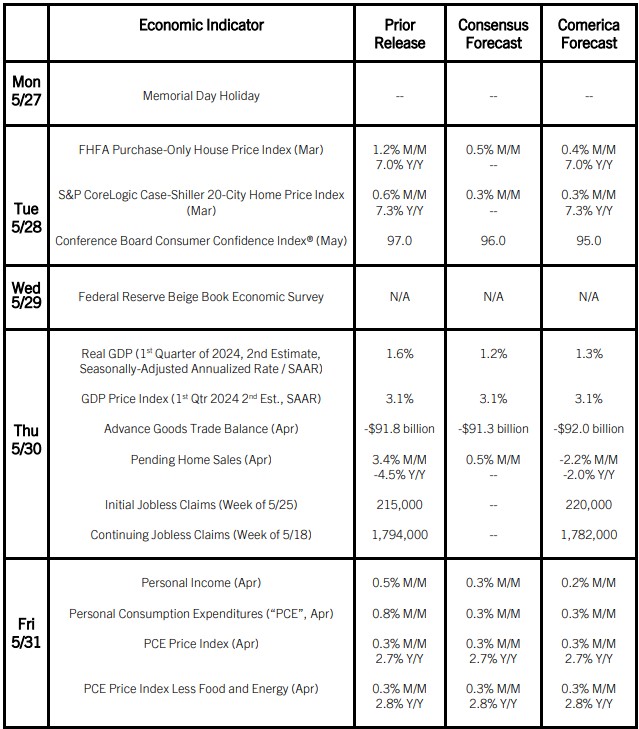

Real GDP growth in the first quarter of 2024 will likely be revised lower in the second estimate’s release, reflecting downward revisions to consumer spending. With the revisions, real GDP growth in the first quarter is expected to be less than half the 3.8% annualized pace of the second half of 2023.

Personal consumption expenditures growth likely slowed in April, and March will likely be revised lower, too. Income growth is expected to slow as well, on slower growth of wage and salary income. The economy’s margin of slack capacity is widening, which will likely contribute to a further slowdown of inflation in the second half of 2024. But April’s inflation data are expected to show price pressures holding steady from March. Total and core inflation by the Fed’s preferred measure, the personal consumption expenditures price deflator, are forecast to be unchanged in both month-over-month and year-over-year terms, both around 2.75%. The Fed targets inflation of 2%.

The Conference Board’s Consumer Confidence Index® likely pulled back in the May release as consumers became less confident in the state of the job market. House price indexes likely rose in March, with their year-over-year pace of increase holding roughly steady. The trade deficit likely widened slightly in April on lower U.S. petroleum exports.

The Week in Review

The minutes of the Fed’s May 1st interest rate decision show some of the rate setting committee’s members are more hawkish than their consensus statement, or than Chair Powell’s guidance in the press conference after the meeting. Lamenting a “lack of further progress” in recent months toward the 2% inflation objective, they were particularly concerned about “significant increases in components of both goods and services price inflation.” Concluding achieving their inflation objective “will take longer than previously thought,” “various” participants expressed willingness to tighten policy further, a very different emphasis than Powell’s statement at the May 1st presser that it is “unlikely the next policy move will be a hike.” “Almost all” FOMC members supported the decision to begin slowing the pace of Fed’s balance sheet runoff. But “various” participants emphasized that balance sheet decisions had no implications for the outlook of interest rate policy. Policymakers judged the economy was expanding at a “solid” pace, but expected economic growth to moderate as the year progresses. Policymakers continue to judge demand and supply are coming into better balance in the labor market.

The housing market weakened in April. Existing home sales, which account for most homes sold in the U.S., fell by 1.9% on a monthly and annual basis. Despite weaker volumes, the median price of houses sold rose for the tenth consecutive month by 5.7% to $407,600, a record for April. On a positive note, the number of houses listed for sale rose to 3.5 months of supply, the most since last November. New home sales fell as well, down 4.7% on the month and 7.7% from a year earlier. The median price of a new home sold fell by 1.4% in April to $433,500, but was 3.9% higher from a year earlier. The number of new homes for sale rose in April to the equivalent of 8.5 months of supply at last months’ sales rate in non-seasonally-adjusted terms, or 9.1 months after adjusting for seasonal variations.

For a PDF version of this publication, click here: Comerica Economic Weekly, May 28, 2024

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.