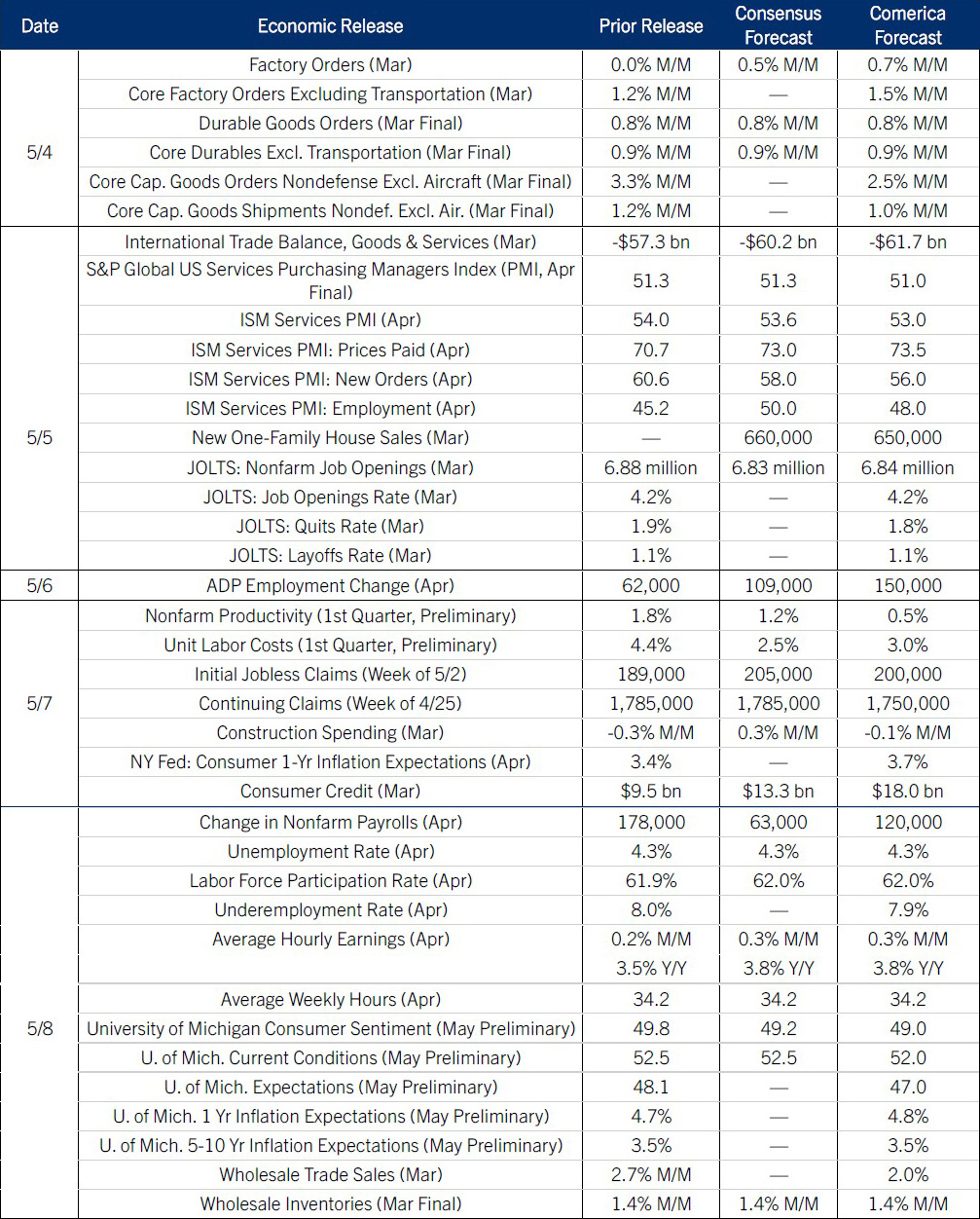

Preview of the Week Ahead

Employers likely added jobs at a moderate pace in April, holding the unemployment rate steady at a goldilocks level of 4.3%. Wage growth likely picked up in year-over-year terms, though not enough to offset higher inflation. It won’t be possible to judge that precisely until next week, when the April CPI report is published. Other labor market data scheduled for release this week are likely to be solid: Job openings likely ticked higher in the delayed March release, and the employment sub-index of the ISM Services PMI likely improved in April.

The Week in Review

As expected, the Federal Open Market Committee held the federal funds target steady at a range of 3.50% to 3.75% on April 29th, the final decision of Jerome Powell’s term as chair. The Fed cut rates by a quarter percentage point in December, and has held them steady at three consecutive meetings since then. Their statement signals they will likely hold the target rate unchanged for the next few decisions while they monitor the economic effects of the Iran war. The vote was 8-4. Governor Miran dissented again in favor of a cut. More notably, three regional Fed presidents supported the rate decision but their dissent is striking because the statement’s language was not especially dovish. It said the Committee would consider the “extent and timing of additional adjustments” by assessing “incoming data, the evolving outlook, and the balance of risks.” What easing bias? “Adjustments” could mean hikes! Their dissent is best understood as a gesture underscoring the Fed’s independence from political pressure to cut rates.

Powell also acted to bolster the Fed’s independence. He will stay on as a governor until the investigations and legal challenges involving the Fed are resolved. His term as governor continues until January 2028, so his delayed retirement blocks the President’s appointment of a replacement with more appetite for low rates. Kevin Warsh will almost certainly be chair by the Fed’s next meeting in June, but the rest of the Fed’s leadership will maintain a high bar for rate cuts. For markets, the drama around the April decision modestly lowers the odds of cuts later this year. But the Mideast War and its implications for petroleum prices are more important factors for the rate outlook.

Real GDP grew 2.0% at an annualized pace in the first quarter of 2026, supported by a record-high contribution from AI-related fixed investment: computing equipment and peripherals, software, and research and development. Real consumer spending grew at a slower pace as the war raised energy prices; harsh winter weather was another headwind. Inflation overshot the Fed’s target again, as measured by the PCE price deflator.

The Conference Board’s Consumer Confidence Index rose to 92.8 in April from an upwardly-revised 92.2 in March, and was slightly below its long-run average. The contrast with the University of Michigan’s Consumer Sentiment Index is striking, since the latter indicator fell to a record low in April. The University of Michigan’s survey has been weaker than other measures of consumer attitudes in recent months due to its higher sensitivity to inflation; The Conference Board’s measure likely provides a better signal of consumers’ spending intentions. Price pressures worsened in April: The ISM Manufacturing PMI reported the highest increase in input prices since 2022, and AAA reported a new four-year high in unleaded gas prices at the pump for American drivers.

For a PDF version of this publication, click here: Comerica Economic Weekly, May 4, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.