Preview of the Week Ahead

The minutes of the Fed’s April meeting are unlikely to surprise markets: With the Iran War pushing up inflation but also clouding the growth outlook, FOMC members mostly agree they should hold rates steady near-term. Their guidance may be more circumspect than usual out of courtesy to incoming Chair Warsh, who will want to make a mark on the Fed’s communication at upcoming meetings even if he doesn’t try to change rates. In any case, the war and energy prices will influence the rate outlook more than the Fed leaders’ baton pass.

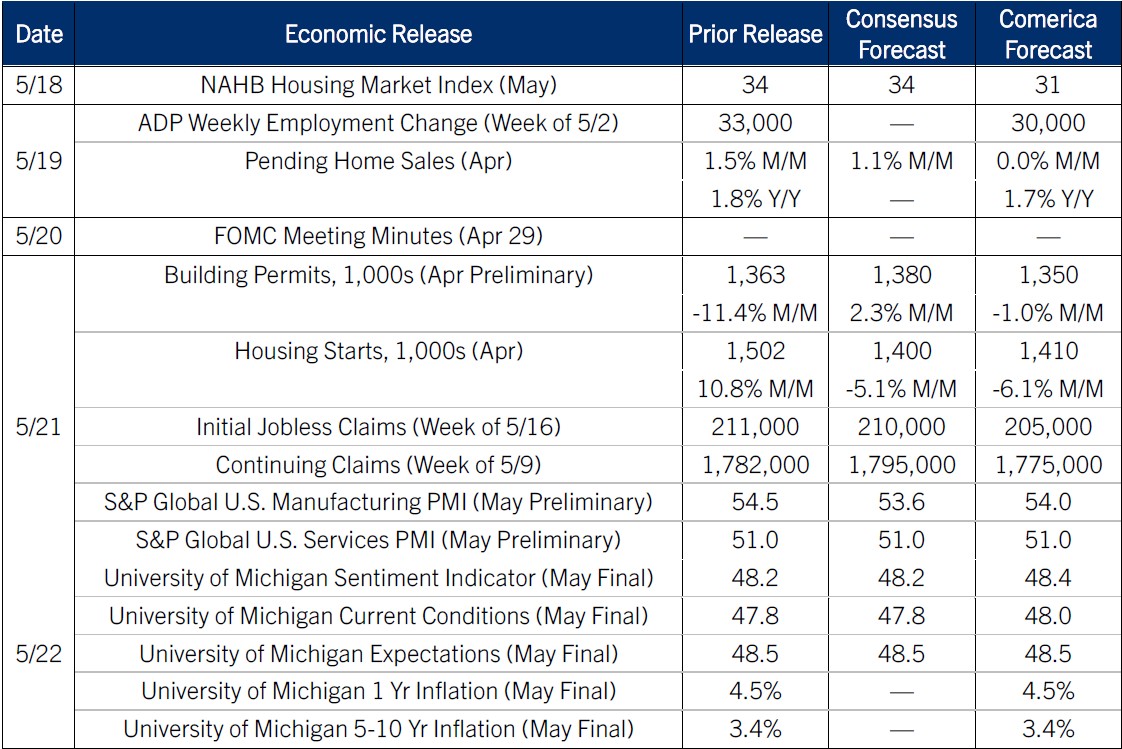

Housing data likely softened further in April as interest rates rose. The National Association of Homebuilders’ survey likely fell, along with housing starts and building permits. Pending home sales, a leading indicator of existing sales, likely held steady after March’s big increase.

The University of Michigan’s Consumer Sentiment Index will likely be revised a bit higher in the final May release, but remain the lowest in the survey’s nearly 50-year history. Consumer inflation expectations likely held near April’s elevated levels. AAA reports the national average gas price reached another four-year high in early May.

The Week in Review

Inflation flared to the worst since 2022 last month. The CPI jumped 0.6% from March and accelerated to a 3.8% annual increase from 3.3% in March as gasoline jumped nearly 30%. New vehicle prices edged up 0.2% on the year, used car and truck prices fell 2.7%, while auto parts and equipment prices rose 3.8%. Shelter costs jumped to a 3.3% annual increase from 3.0% in March as the Bureau of Labor Statistics incorporated survey data delayed by last year’s government shutdown. This raised core CPI excluding food and energy to 2.8% from 2.6% in March.

Producer price inflation was even worse. The PPI jumped 1.4% with energy up 7.8% and transportation and warehousing costs up 5.0%. In annual terms, PPI accelerated to 6.0% from 4.3% in March and was, like CPI, the highest since 2022. Core PPI excluding foods and energy rose to 5.2% from 4.0%, and core PPI excluding foods, energy and trade services rose to 4.4% from 3.7%. Both measures of core PPI were the highest since 2023.

The first activity indicators for April were more encouraging. Retail and food service sales rose 0.5%, or 0.3% excluding the 2.8% jump in gas station sales. Discretionary spending categories were mixed. To the upside, electronics and appliance sales rose 1.4%, sporting goods, hobby, musical instrument and book sales rose 1.4%, and nonstore retail (mostly e-commerce) rose 1.1%. To the downside, motor vehicle and parts dealer sales fell 0.4%, clothing and clothing accessory sales fell 1.5%, and furniture and home furnishing sales fell 2.0%. Grocery store sales rose 0.7%, while food service and drinking place sales rose 0.6%.

The real bright spot last week was the industrial production report. IP jumped 0.7% in April on a 0.6% increase in manufacturing and a 1.9% surge in utilities. Mining edged down 0.1%. Motor vehicle and parts production rose 3.7% as the motor vehicle assembly rate recovered to the highest since August. Aerospace product and parts production was up 2.1%, and up 9.0% on the year to the highest level of output since 2018. Petroleum refinery output rose 2.1% and reached the highest level since 2020. Electricity output rose 1.1% and is up 2.0% on the year; it is slightly below December’s record high.

For a PDF version of this publication, click here: Comerica Economic Weekly, May 18, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.