Preview of the Week Ahead

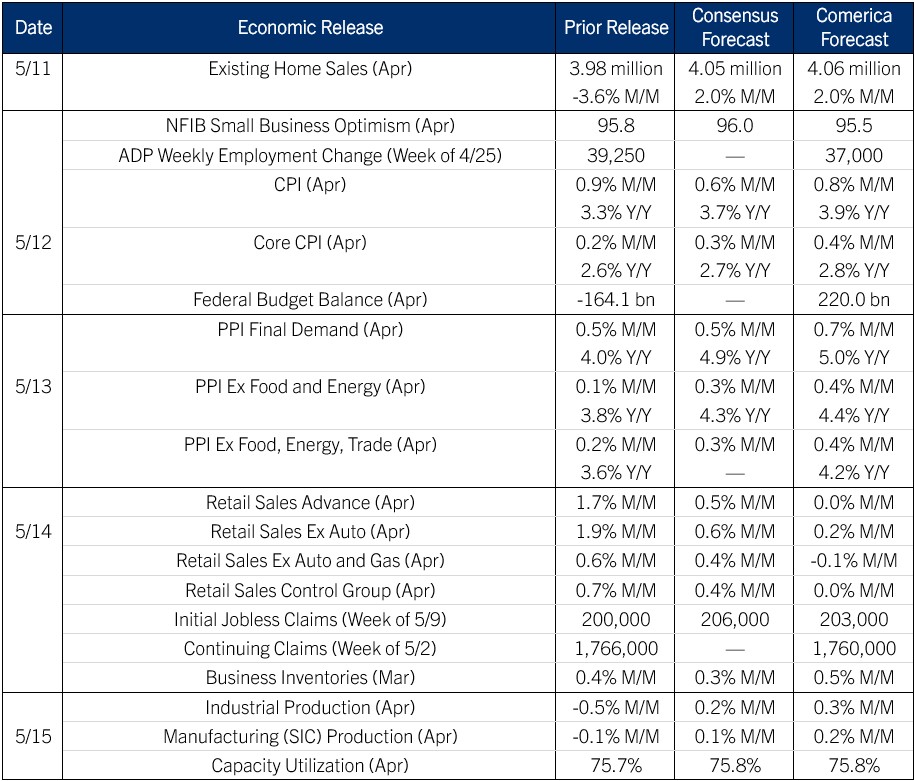

This week’s CPI release is forecast to show headline inflation rose toward 4% in April and reached the highest in nearly two years, pushed up by higher gas prices. Core CPI is also forecast to pick up on the month on a hot shelter print. Part of that reflects mechanical catch-up from the gap in shelter price data during last year’s government shutdown. PPI likely accelerated to the fastest since early 2023 in April.

The April retail sales report will likely come in soft, with consumers spending more at gas stations while reining in discretionary spending elsewhere. Industrial production likely fared better, rising moderately. Existing home sales likely rebounded in April after March’s drop, and are trending similarly to their pace last year. The median existing home’s sale price likely rose in the low single digits from a year ago. The federal budget is forecast to swing to a surplus in April, but a smaller one than a year ago as tax cuts reduce revenues, and as spending increases on defense and domestic security programs.

The Week in Review

Labor demand improved in the April jobs report, while supply tightened. On the demand side, nonfarm payroll employment rose 115,000, above the 65,000 consensus and near Fifth Third Commercial Bank’s 120,000 forecast. February and March were revised down a net 16,000. After revisions, payrolls averaged a 76,000 monthly increase year to date, up considerably from 10,000 per month last year. By major industry, healthcare and social assistance added 54,000 jobs, transportation and warehousing 30,000, retail 22,000, and leisure and hospitality 14,000. In goods-producing sectors, manufacturing edged down 2,000, construction rose 9,000, mining and logging added 3,000. Government employment fell 8,000.

The unemployment rate held steady at 4.3%, matching both our forecast and the consensus, and was down from 4.5% last November. In the volatile household survey, employment fell 226,000, the labor force contracted 92,000, and unemployed jobseekers rose 134,000. The labor force participation rate edged down to 61.8%, the lowest since late 2021. The labor force is down by over a million from a year ago. The prime-age (25-54) employment-to-population ratio held at 80.7%, just a hair below July 2023’s 80.9% cyclical peak, which was the highest since 2001.

Average hourly earnings rose 0.2% and were up 3.6% on the year. That’s up slightly from March, when they registered the slowest growth of this expansion. Data on the workweek were contradictory, providing no clear signal. Workers who were part-time for economic reasons jumped 445,000, but the average workweek also lengthened a tenth of an hour to 34.3 hours. Aggregate hours worked rose 0.3% and aggregate payrolls 0.6%.

The labor market is inching out of last year’s low-hire/low-fire mode into moderate-hire/low-fire. That’s reassuring amid elevated anxiety tied to the Iran War. The job market is riding tailwinds from tax cuts, higher public spending, and the Fed’s rate cuts in late 2025. Also, firms are catching up on hiring and capex they delayed during last year’s tariff uncertainty. With hiring stronger but participation falling, the labor market seems set to tighten this year if the economy avoids downside risks from the Iran War. For the Fed, firmer payrolls growth alongside a shrinking labor force argue against a rate cut at Kevin Warsh’s first meeting as chair next month.

For a PDF version of this publication, click here: Comerica Economic Weekly, May 11, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.