Preview of the Week Ahead

The March jobs report is forecast to show employers added jobs during the month after a drop in February, but that the unemployment rate edged up as more job seekers entered the labor force. The Conference Board’s Consumer Confidence Index likely pulled back in March on higher gas prices and stock market volatility. The news flow likely pushed down consumers’ views of the job market to the weakest since 2021.

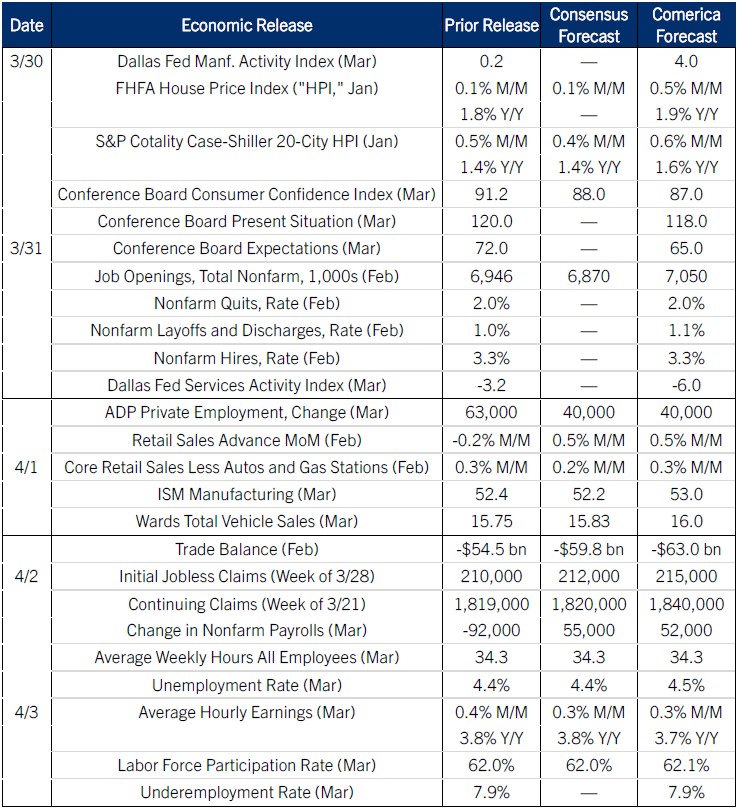

House price increases likely accelerated in January after 2025 ended with gains of 1.5% to 2.0% percent, lagging incomes and household wealth. Housing affordability is gradually improving, although the recent uptick in mortgage rates is a new headwind for potential buyers.

Retail sales likely rebounded in February on higher new and used auto sales after harsh weather weighed on January sales. Individual income tax refunds are up 12.5% so far this year. Core retail sales likely rose moderately in February. Consumer spending was in good shape before the Iran War, but discretionary spending likely will look more cautious in the next release for March.

The Week in Review

The manufacturing purchasing managers index (PMI) published by S&P Global rose to 52.4 in the March flash release, above its 2025 average level. Supplier delivery times lengthened by the most since late 2022 as the Iran war disrupted shipping in the Middle East. Selling prices also jumped as businesses passed through higher petroleum costs. The S&P Global Services PMI pulled back to 51.1 from 51.7 and was the weakest since Liberation Day in April 2025.

The University of Michigan’s Consumer Sentiment Indicator was revised down to 53.3 in the March final release from 56.6 in February. Consumers’ views of the economic outlook deteriorated, as did their views of personal finances. Homebuying conditions were a silver lining of the report: They edged lower on the month but were still near the highest since early 2024. Consumers have noticed increased listings and price cuts in many major property markets. The Iran war is dominating headlines now, but if it calms down, 2026 is likely to see a pickup in home sales, especially in the existing-home market.

In speeches last week, several Fed governors and regional Federal Reserve Bank presidents said that the Fed should take a wait-and-see approach toward responding to the Iran War. Policymakers mostly agree that the war would have to grind on for an extended period to justify rate hikes. On the other hand, they mostly agree that rate cuts are off the table while energy prices are surging. Several mentioned they still think cuts are possible this year.

An oil refinery explosion added to upward pressure on diesel prices last week. The spread of diesel prices over WTI crude widened to roughly 20% above its average over the last five years. Diesel averaged $5.32 per gallon at U.S. pumps late last week, while average gasoline prices held a few cents below $4 per gallon.

For a PDF version of this publication, click here: Comerica Economic Weekly, March 30, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.