Preview of the Week Ahead

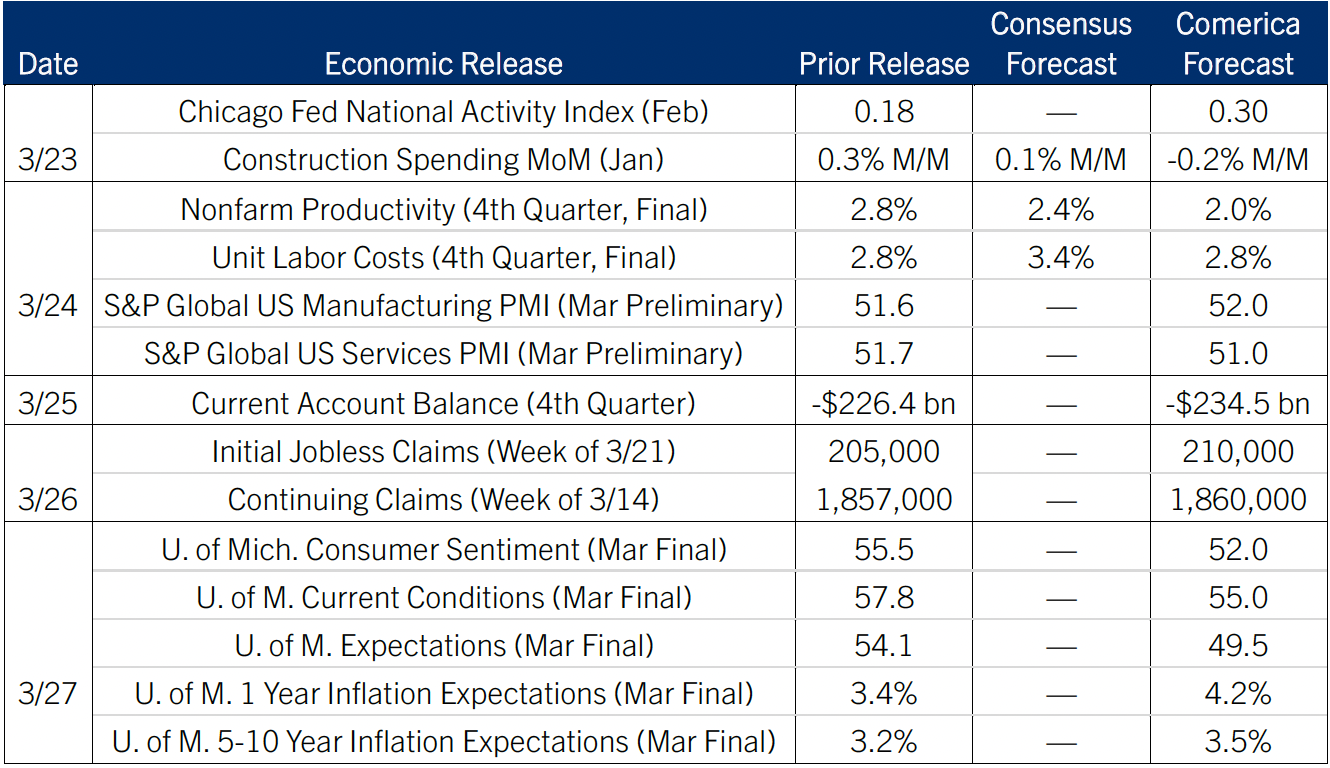

Surveys out this week will provide an early read on the reaction from businesses and consumers to the war with Iran. For businesses, the preliminary releases of S&P Global’s purchasing managers indexes (PMIs) are the first major data on sentiment since the outbreak of hostilities. They will likely report faster increases in input costs as prices for diesel, jet fuel, fertilizer, and other petroleum products spike. Business order books will receive more attention than usual.

For consumers, the final release of the University of Michigan’s consumer sentiment indicator will give a clearer read on reactions to rising gas prices and tumultuous headlines. The indicator likely closed the month lower than in its preliminary release as expectations for personal finances weakened, and as inflation expectations rose. Consumers’ views of their current financial situation may have held up better, since income tax refunds are up 12% on the year so far this tax season.

The Week in Review

The Iran war pushed diesel above $5 per gallon at pumps across the U.S. last week according to AAA, the highest since late 2022 on a national average basis. Gasoline also reached the highest since 2022, a few cents shy of $4 per gallon. As retail energy prices rise, so do inflation expectations: The spread between the nominal 1-year U.S. Treasury yield and the inflation-indexed yield widened to over 5.2% last week, also the highest since 2022.

The Fed signaled a “wait-and-see” approach to responding to the war at their March 18 decision. As was all but assured, they held rates unchanged. The members of the Federal Open Market Committee (FOMC) raised their forecasts for inflation, but played down the importance of forecasts in such a rapidly changing situation. Chair Powell remarked after the meeting that “a number of [FOMC members] mentioned if we were ever to skip an SEP [Dot Plot], this is a good one.” For what it’s worth, the Dot Plot shows fewer FOMC members thought more than one rate cut would be appropriate by year end 2026. On the other hand, no members think a hike would make sense, either; three members favored a hike in 2026 in last December’s Dot Plot. The two-year and 10-year Treasury yields rose to the highest since last summer on higher U.S. inflation expectations, as well as spillover from turbulent financial markets in Europe, where the energy supply shock is a bigger blow to the economy. The 30-year fixed mortgage rate rebounded to the highest since late 2025 after dipping below 6% in February.

The February release of the producer price index (PPI) showed businesses faced substantial inflationary pressures even before the war broke out. The PPI rose 0.7% from January, overshooting the 0.3% consensus. Foods prices rose 2.4%, and energy prices 2.3%. Core goods excluding foods and energy rose 0.3%. Final demand services rose 0.5% on big increases of trade services (wholesale and retail margins), up 0.4%, transportation and warehousing, up 0.5%, and of other services, up 0.6%. PPI inflation was 3.4% in annual terms, while core PPI inflation excluding foods and energy was 3.9%, a tie for the highest since early 2023. Household net worth rose $2.2 trillion in the fourth quarter of 2025, up 8.8% from a year earlier. Growth of wealth continues to outpace incomes—disposable personal income rose 4.2% in the same period.

For a PDF version of this publication, click here: Comerica Economic Weekly, March 23, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.