Preview of the Week Ahead

The Fed will hold rates steady at Wednesday’s meeting and signal vigilance toward inflation rising due to the Iran war. Ordinarily, central bankers try to look through the impact of an inflationary shock to energy prices and other events disconnected from the business cycle, since inflation usually returns to trend once shocks subside. But this shock follows half a decade of inflation overshooting the Fed’s target, so they will be attuned to the risk that consumers’ and businesses’ inflation expectations follow prices at the pump higher. The March dot plot will likely raise the forecast for inflation and signal that the median member of the Federal Open Market Committee expects to hold rates steady through the end of 2026.

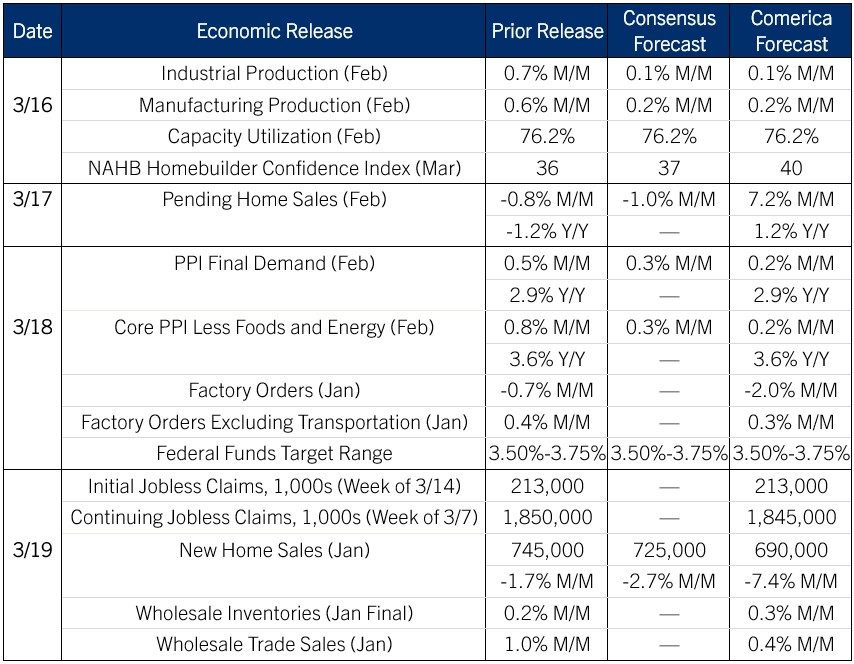

Industrial production likely grew slower in February after January’s cold weather boosted utilities output. Manufacturing growth was likely moderate and capacity utilization is forecast to hold steady. Producer Price Index inflation likely held steady in February. It will rise in March on the surge in prices of diesel, gasoline, and other petroleum products after the outbreak of the war.

The Week in Review

National average diesel prices at the pump surged 30% from February 28 to March 13, and gasoline prices rose more than 20%.

CPI inflation held unchanged at 2.4% in February while the Fed’s preferred measure of inflation, the PCE price index, rose 2.8% on the year in the delayed January release. Like the PPI, these measures of inflation will jump in March as higher prices of energy, airfares, and shipping services push up the price basket.

Job openings rose to 6.946 million in January from 6.550 million in December, which was the lowest since 2021; openings are still weak. Layoffs and quits both fell in January.

The University of Michigan’s consumer sentiment indicator pulled back to 55.5 in the March preliminary release from 56.6 in February as consumers fretted about the war. The University of Michigan noted that surveys collected after the war’s outbreak reported higher inflation expectations and weaker expectations for personal finances.

Real GDP in the fourth quarter of 2025 was revised down in the second estimate to a 0.7% annualized increase from 1.4% annualized in the first estimate. The downward revisions were concentrated in consumer spending on services, business fixed investment in structures, and exports. Core real GDP (Final sales to private domestic purchasers) was revised down to 1.9% annualized from 2.4% annualized previously. In January, personal consumption expenditures rose 0.4% but were up just 0.1% after adjusting for inflation; January was the third consecutive month with such weak real consumer spending. Personal incomes also rose 0.4%. Real disposable personal income rose 0.7% as personal current taxes fell 3.2%, reflecting the effect of tax cuts passed last year that came into effect on January 1. From a year earlier, real disposable personal income rose 1.8% and real personal consumption expenditures rose 2.4%.

For a PDF version of this publication, click here: Comerica Economic Weekly, March 16, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.