Preview of the Week Ahead

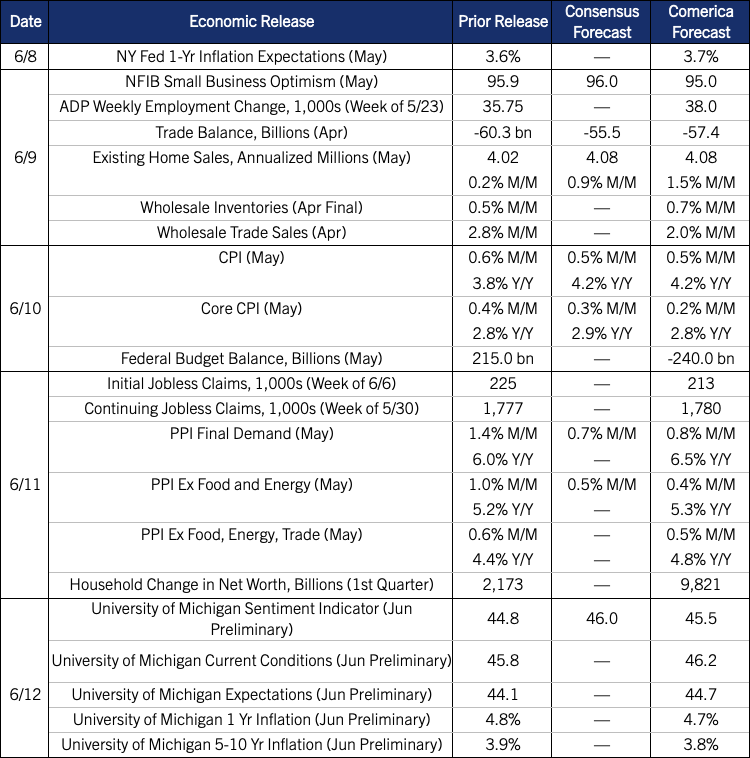

Headline CPI is expected to top 4% year-over-year in the May release, reaching a three-year high on last month’s rise in gasoline prices. Core CPI should run cooler, near 3% year-over-year. Prices rose faster than average hourly earnings in May, eroding consumers’ purchasing power. The PPI likewise registered another outsize increase and outpaced the CPI, reflecting the larger shares of petroleum products, metals, and shipping costs in the producer price basket.

Consumer inflation expectations are likely to tick higher in the New York Fed’s May survey, weighing on views of the economy and job market. But the University of Michigan’s more timely read on consumer sentiment for early June will likely edge up from May’s record low, helped by lower gasoline prices over the last two weeks and higher stock prices.

The Week in Review

Employers added a solid 172,000 jobs in May, well above the 88,000 consensus and our forecast of 85,000. Job growth was concentrated in leisure and hospitality, up 70,000, local government, up 55,000 and health care and social assistance, up 47,000, three industries that are relatively insulated from the effects of AI. The unemployment rate held steady at 4.3%. In the survey of households, the labor force rose 83,000, but was down 414,000 on the year, equivalent to 35,000 per month. The economy has added 114,000 jobs per month so far in 2026, up from a paltry 10,000 per month last year. This trend could lower the unemployment rate in the second half of 2026 if sustained, and even cause labor supply bottlenecks by next year. That would pressure the Fed to raise rates even if the inflation shocks from the Iran War and tariffs fade. But for now, the risk is hypothetical: A 4.3% unemployment rate isn’t a call to action for the Fed. The May jobs report has no sign of wage-price pressures—in fact, average hourly earnings tied for the slowest year-ago increase since the expansion took off in 2021, lagging the CPI for a second straight month. The lagged release of the Job Openings and Labor Turnover Survey (JOLTS) for April showed green shoots for hiring in months ahead, with openings jumping to the highest since mid-2024. Other parts of the JOLTs report were still cool, though, with hires, quits, and layoffs/discharges rates edging lower.

The ISM Manufacturing and Services PMIs both strengthened in May: The Manufacturing PMI rose from 52.7 to 54.0, its highest in four years (Relatedly, factory orders jumped 4.8% in April and were up 11.7% on the year). The Services PMI rose to 54.5 from 53.6 and was near the top of its range since 2022. Input price pressures remained intense in both surveys, with manufacturing prices rising slower than in April but services prices accelerating. The surveys report ongoing supply bottlenecks from the Iran War, as well as shortages of semiconductors, computers, and other equipment in high demand due to the AI boom. Both surveys reported employment lower on the month.

Car and light truck sales recovered to a 16.08 million annualized rate in May. That strength, together with the strong May jobs report, suggest May’s record low from the University of Michigan’s Consumer Sentiment Index likely overstates the downside risk to consumer spending.

For a PDF version of this publication, click here: Comerica Economic Weekly, June 8, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.