The Week Ahead

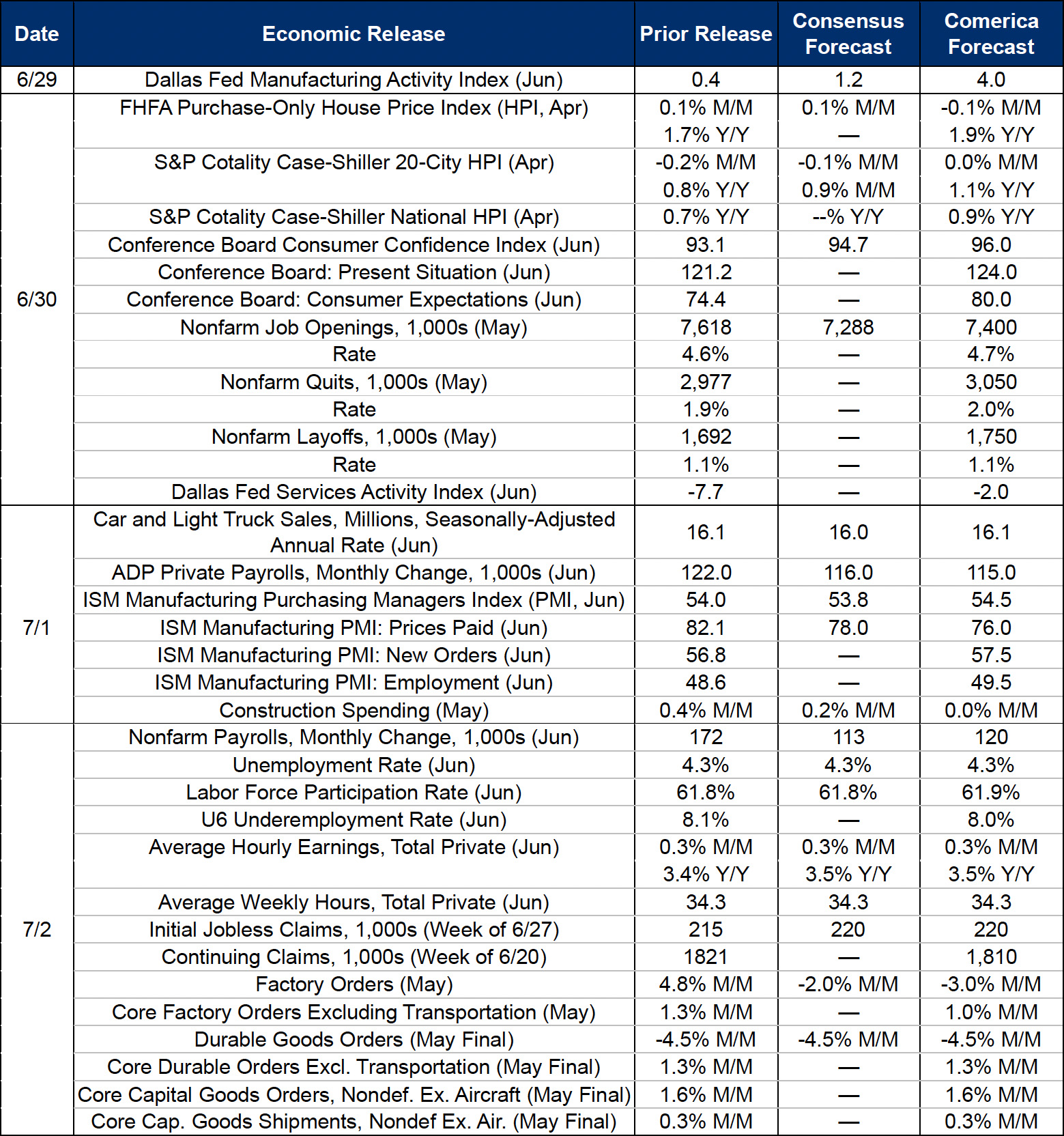

The June jobs report is forecast to show that employers added more than 100,000 jobs again last month, holding the unemployment rate roughly steady near four and a quarter percent. The volatile survey of households will likely show the labor supply held about flat in the first half of 2026, restrained by an aging population and tighter immigration policies. The June jobs report won’t reflect the effects of the U.S.-Iran de-escalation, since its surveys cover the period before the deal was announced. One especially useful detail in the household survey will be unemployment among workers aged 20 to 24 with no prior work experience (Largely the Class of 2026). It likely pulled back relative to June 2025, when it tied 2020 for the highest June since 2016.

Consumer confidence is forecast to rise in June on the month’s decline in gas prices. Inflation expectations should fall and vacation intentions improve, good tidings for the rest of the summer travel season.

Last Week in Review

The personal consumption expenditures (PCE) price index rose 0.4% in May (0.4498% before rounding), near the 0.5% consensus. From a year earlier, PCE inflation picked up to 4.1% from 3.8% and reached the highest since May 2023, matching expectations. Gasoline and other energy goods were the biggest culprit behind higher inflation, jumping 6.5%. But price pressures extend beyond just energy. The core PCE index excluding food and energy rose 0.3% (0.3201%) and ticked up to a 3.4% year-over-year increase, the highest since October 2023, from 3.3% in April. The Supercore PCE index—Service prices excluding energy and housing—rose 0.5% and 3.9% from a year earlier, the highest since December. And the market-based PCE index excluding food and energy, another measure of core inflation, rose 3.2% and reached the highest since November 2023. May’s higher core inflation bolsters the case for the Fed to hike rates over the next 12 months. But the FOMC will likely hold them steady again at the next decision on July 29, since inflation shocks from tariffs and the war are fading and could bring down core inflation by the fall.

Personal income and personal consumption expenditures both jumped 0.7% in May, stronger than consensus forecasts. Adjusted for inflation, real personal consumption expenditures rose 0.3%. After taxes and inflation, real disposable personal income rose 0.3% after declines in each of the prior three months. The personal saving rate tied April for the lowest since June 2022, underscoring the strain on household budgets.

Real GDP in the first quarter was revised up to a 2.1% seasonally adjusted annualized rate from 1.6%, but the details were weaker than the headline: Real personal consumption expenditures were revised down to a 0.5% annualized rate from 1.4% and registered the weakest increase in four years. A big downward revision to imports narrowed the trade deficit and boosted GDP, while nonresidential fixed investment was revised up. Our preferred measure of core real GDP, real final sales to private domestic purchasers, was revised down to 1.7% annualized from 2.4%. Even after the downward revision, the first quarter’s pace was fast enough for the economy to absorb new labor force entrants and keep the unemployment rate steady. Just as important, the outlook for the rest of the year has improved now that energy is flowing through the Strait of Hormuz again.

For a PDF version of this publication, click here: Comerica Economic Weekly, June 29, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.