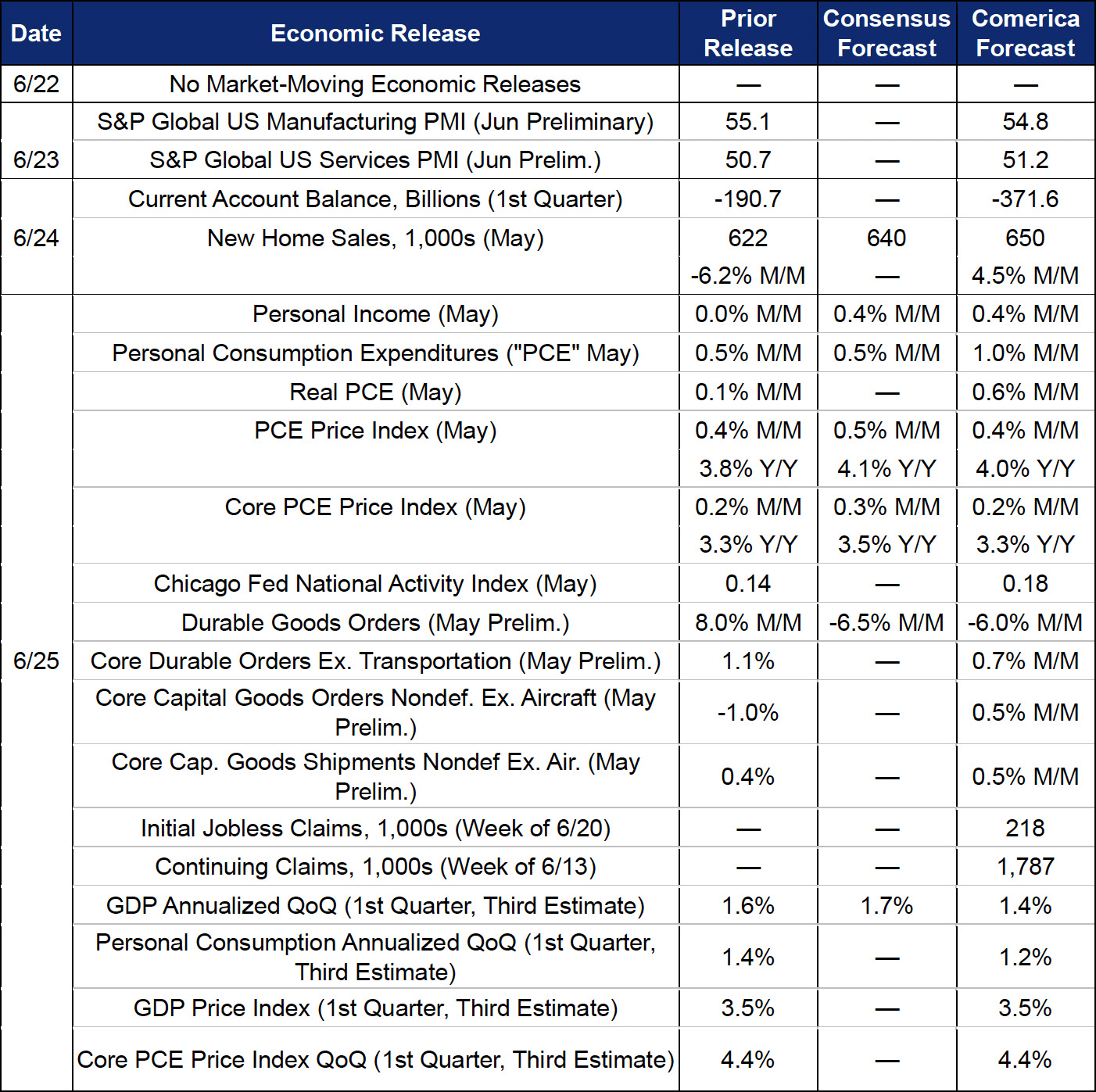

The Week Ahead

The Fed’s preferred measure of inflation is forecast to rise to the highest in three years in the May release, reflecting the same spike in energy prices that pushed up the CPI and PPI during the month. Energy prices fell in the first half of June, which should lower PCE inflation considerably in the next report.

Consumer sentiment is expected to be revised higher in the final release for June, bolstered by recent weeks’ drop in gasoline prices and buoyant stock markets.

Real GDP growth in the first quarter of 2026 is forecast to be revised down slightly in the Bureau of Economic Analysis’s third estimate, incorporating recent data that pointed to softer consumer spending on services and business fixed investment in equipment.

Last Week in Review

As expected, the Fed held the federal funds target unchanged at a range of 3.50% to 3.75% at the June 17 decision, Chair Kevin Warsh’s first at the Fed’s helm. The vote was unanimous. The June decision dramatically shortened the policy statement, dropping most forward guidance—though it retained a restatement of the Fed’s commitment to stable prices and maximum employment, and a separate restatement that “The Committee will delivery price stability.” As expected, the June Dot Plot indicated the question facing the FOMC has shifted from “should we cut” at the start of 2026 to “should we hike.” The Dots were about evenly split between FOMC members supporting a hike by year-end and those supporting no change. This implies that the dominant view of voting FOMC members represented by the Dot Plot is unchanged rates—the most hawkish voices on the FOMC are the regional Fed presidents, and only a subset of them get to vote on decisions. However, the Dot Plot carries less weight than in the past since Chair Warsh refrained from submitting forecasts to it. His skepticism of forward guidance extends to the Dot Plot, which he clearly plans to phase out. Financial markets interpreted the decision as raising the odds of rate hikes over next 12 months, in part because there is no sign that the Fed is paying any more attention to political pressure to cut rates than it did under former Chair Powell’s leadership.

The U.S. and Iran announced last week they will reopen the Strait of Hormuz to energy shipping, greatly diminishing risks to the U.S economic outlook. U.S. crude oil futures fell to the lowest since early March on the news. The peace deal has offsetting impacts on the two legs of the Fed’s dual mandate for stable prices and maximum employment, since it reduces downside risks to the job market (less reason for the Fed to cut) and also reduces upside risks to inflation (less reason to hike).

The first activity indicators for May were mostly positive. Retail sales were stronger than expected, up 0.9% on the month, with core sales excluding gas stations and autos up 0.5%. Industrial production was cooler, rising a smaller-than-expected 0.1% on the month with manufacturing production flat. Revisions lowered production in the first quarter. Housing data were mixed, with the NAHB Housing Market Index pulling back in May to the second-lowest since last September, while pending home sales rose during the month.

For a PDF version of this publication, click here: Comerica Economic Weekly, June 22, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.