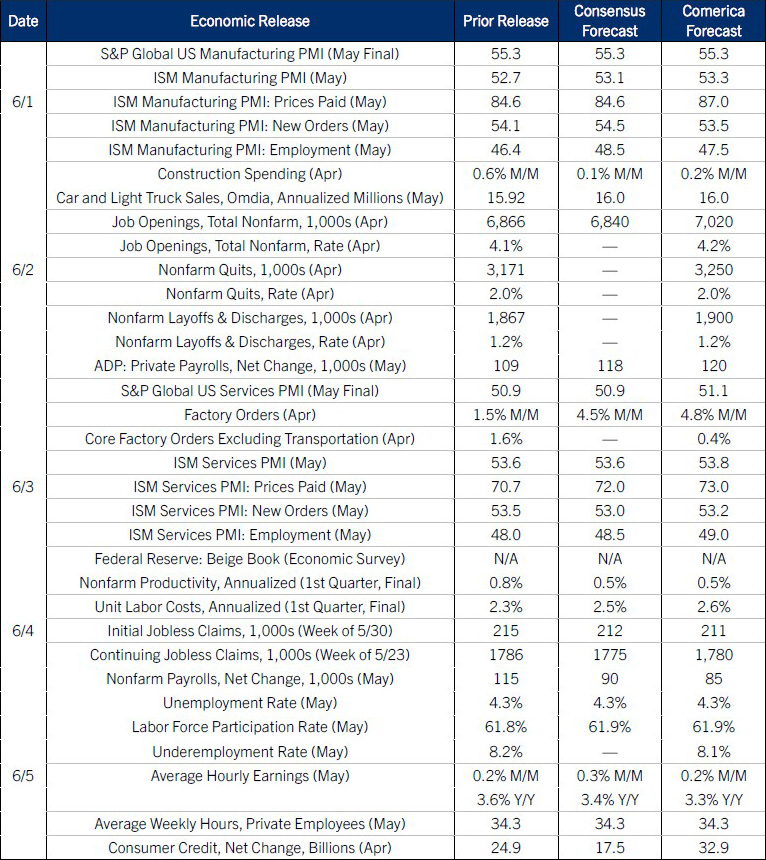

Preview of the Week Ahead

Payrolls will likely rise modestly in the May jobs report, but still outpace labor supply growth. An aging workforce and immigration restrictions mean fewer workers are entering the labor force. The unemployment rate is expected to hold steady. Average hourly earnings likely rose modestly and slowed on a year-over-year basis. The lagged release of the April Job Openings and Labor Turnover Survey is expected to show higher openings, with layoffs and quits rates holding steady. The ISM manufacturing and services PMIs are both forecast to edge up in May’s releases. The surveys are also likely to show intensifying margin pressure as higher petroleum prices lift input costs.

The Fed’s Beige Book will likely highlight a widening gap between spending by affluent households and middle- and lower-income households—The K-shaped economy—as higher energy prices squeeze the cost of living.

The Week in Review

The PCE price index—the Fed’s preferred inflation gauge—jumped to 3.8% year over year in April from 3.5% in March and was the highest in nearly three years. It was up 0.4% from March. Core PCE wasn’t as bad, up 0.2% on the month, but its 3.3% year-ago increase was still well above the Fed’s target. PCE Services prices excluding energy and housing (“Supercore PCE”) rose 0.1% on the month and 3.5% on the year.

Consumer spending rose as households paid more at the pump, but real spending was nearly stagnant. Personal consumption expenditures rose 0.5% on the month, led by a 0.4% increase in services. Nondurable goods jumped 1.0% (This category includes gasoline) while durable goods were flat. Adjusted for inflation, real goods spending edged down 0.1% while real services rose 0.2%.

Personal incomes were flat on the month, weighed down by the expiry of a farm subsidy program. Other categories were mostly better, with wages and salaries up 0.2%, dividends up 0.1%, and interest up 0.5%. Adjusted for inflation and taxes, real disposable personal income fell for a third straight month, down 0.5%. The personal saving rate fell to the lowest since mid-2022, the last time energy prices surged, signaling stress on consumer finances. Real GDP in the first quarter of 2026 was revised down to a 1.6% annualized increase in the second estimate from 2.0% in the first estimate, mainly because of downward revisions to investment in inventories and consumer spending. Real final sales to private domestic purchasers—a measure of core GDP—was better, revised down just a hair to 2.4% from 2.5%. Real gross domestic income (Another GDP cross-check) rose a modest 0.9%, down from 2.4% in 2025.

The housing market remains stuck in low gear. New single-family home sales fell 6.2% in April and are down 6.5% year to date. The median price of a new home sold rose 2.2% from a year earlier to $423,000. It’s changed little in the last three years. The S&P Cotality Case-Shiller 20-City Home Price Index slowed to a 0.8% year-over-year increase in March from 0.9% in February, while the FHFA Purchase-Only HPI slowed to 1.7% from 1.8%.

The Conference Board’s Consumer Confidence Index was a little stronger than expected in May, though it slipped from April’s upwardly-revised level. In the survey's details, views of the job market have held about steady since January after trending down in the prior four years.

For a PDF version of this publication, click here: Comerica Economic Weekly, June 1, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.