The Week Ahead

The minutes of the Federal Open Market Committee’s June meeting will draw more scrutiny than usual after Chair Warsh shortened the policy statement and eliminated forward guidance from it. The minutes will likely drop their usual description of policymakers’ opinions about their next step for rates, paralleling the leaner statement. In the absence of forward guidance, the discussion of the inflation outlook has the most potential to influence financial markets’ pricing of the Fed’s next steps.

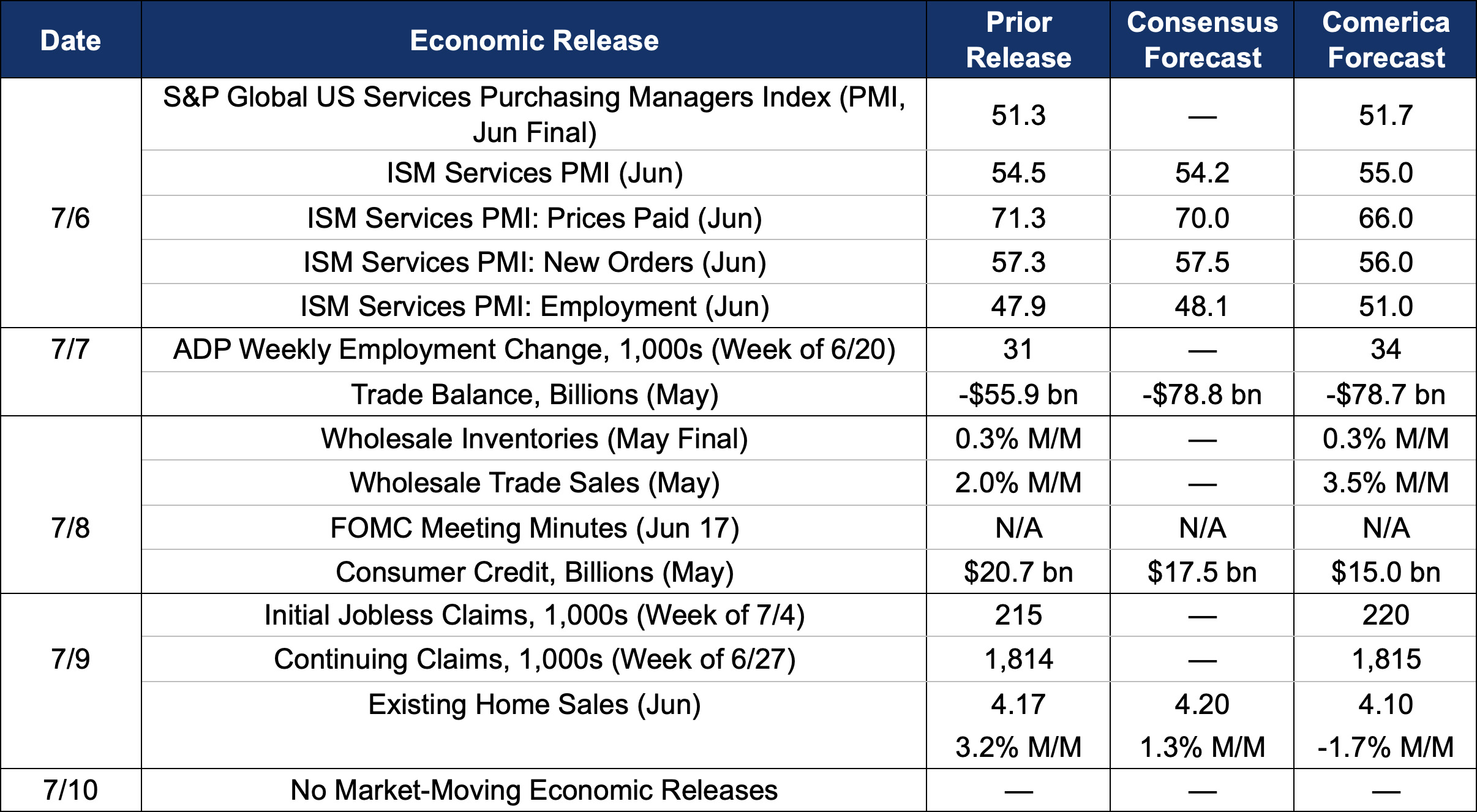

The Institute for Supply Management’s Services Purchasing Managers Index (ISM Services PMI) likely improved in June, with orders increasing faster after energy traffic picked up through the Strait of Hormuz and domestic energy prices receded toward pre-war levels. The PMI’s Employment sub-index likely returned to expansionary territory as the World Cup boosted hiring in leisure and hospitality.

Last Week in Review

Employers added 57,000 payroll jobs in June, down from a downwardly-revised 129,000 in May. A 55,000 drop in accommodation and food services weighed on hiring, surprisingly given anecdotal reports of a good month for the industry during the World Cup. Information shed 9,000 jobs and retail 8,000. Healthcare and social assistance added 47,000 jobs, professional and business services added 36,000 (including 9,000 temp jobs), and private education added 22,000. Government added 8,000, mostly at the state and local level. Incorporating revisions, job growth averaged 111,000 per month in the second quarter and 92,000 per month in the first half, up from 10,000 per month in 2025. Average hourly earnings rose 0.3% and were up 3.5% on the year, near the lowest of the expansion to date. The average workweek held steady at 34.3 hours.

The unemployment rate edged down to 4.2% from 4.3% in June and was the lowest in a year. The U-6 unemployment rate, which includes active jobseekers, people who searched for a job in the last 12 months, as well as those who work part-time but want full-time jobs, edged down to 7.9% from 8.1%. The household survey’s details were very weak: The labor force plunged 720,000, employment fell 507,000, and unemployment fell 213,000. The labor force participation rate dropped to 61.5% from 61.8% and was the lowest since March 2021. A big part of the decline was a 0.6 percentage point plunge in participation among workers aged 25 to 54. Outside the pandemic, that’s the largest monthly drop in nearly 60 years, and could be mostly noise. But participation among other demographics isn’t great, either: The participation rate of workers aged 55 and older tied May for the lowest since 2005. The participation rate for workers aged 16 to 24 was better, edging down a tenth of a percent but still above its level a year earlier. The labor force contracted 119,000 per month in the first half of 2026, but again, the June report probably overstates its weakness somewhat.

The job market trended better in the first half of the year than in 2025’s low-hire, low-fire freeze, which should bolster consumer confidence in the second half of the year. Consumers are fretting about AI fueling big job losses, but that doesn’t seem to be happening. Instead, the job market’s defining theme in 2026 is weak labor supply as older workers retire and fewer immigrants enter the workforce. The unemployment rate will likely continue to move lower in the second half of the year as labor demand outpaces supply. Businesses will likely start noticing job openings taking longer to fill, especially for positions in physically demanding blue collar occupations.

For a PDF version of this publication, click here: Comerica Economic Weekly, July 6, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.