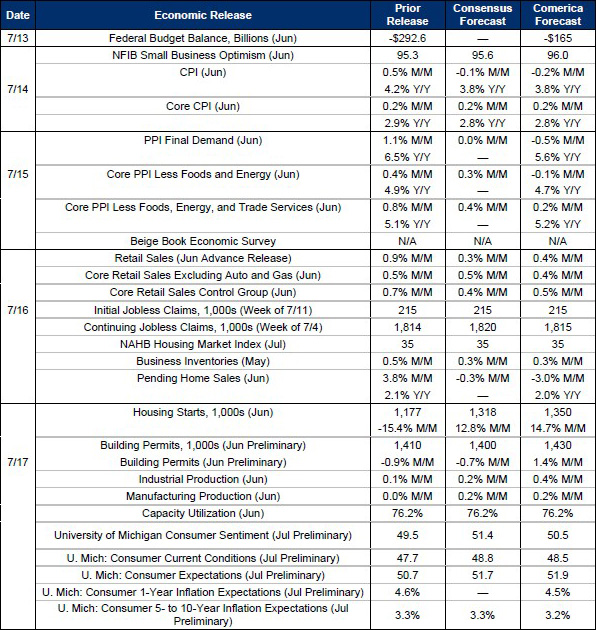

The Week Ahead

CPI inflation likely eased back below 4% in June as energy flows resumed through the Strait of Hormuz, helping U.S. gas and diesel prices reverse part of their spring surge. PPI inflation, which is more sensitive to energy prices than the CPI, likely slowed as well, moving back below 6%. However, core CPI and PPI likely improved less and probably continue to run above levels consistent with the Fed’s 2% inflation target, which is measured by the PCE price index (PCE averages about a quarter percentage point below CPI over the long run). Last week’s re-escalation of the Iran conflict pushed U.S. energy prices modestly higher, potentially obstructing further progress toward lower inflation in July.

Last Week in Review

The minutes of the Fed’s June meeting removed explicit forward guidance about interest rates, mirroring the slimmed-down policy statement released immediately after the meeting. Without guidance, financial markets focused on the minutes’ description of risks to the Fed’s dual mandate of stable prices and maximum employment: “Upside risks to price stability remained elevated while downside risks to achieving maximum employment had moderated a bit.” Along with “a few” FOMC members seeing “a case” for hiking rates in June, financial markets interpreted the minutes as further evidence that hikes are likely over the next 12 months.

The minutes project more ambiguity about the rate outlook than market pricing implies. They describe a Fed that is more data-dependent than outright hawkish. In a paragraph describing future options for interest-rate policy, “most” FOMC members mentioned both upside and downside inflation scenarios. Among members who laid out these scenarios, “almost all” thought hikes make sense if inflation runs hot, while they should “maintain or eventually lower” rates if it runs cool. Does that sound like a hiking bias, or “On the one hand, on the other hand?”

The Institute for Supply Management’s Services PMI edged down to 54.0 in June from 54.5 in May, but still indicated solid growth among service-providing businesses. The Employment sub-index rebounded to 51.2 from 47.9, in line with Fifth Third Commercial Bank’s above-consensus forecast and the first expansion reported since February. The Prices Paid Index still points to elevated inflation pressures, but receded to the least since February and matched its average in the second half of 2025.

Existing home sales fell 2.4% in June, but were still up 2.2% in the first half of 2026 from 2025’s depressed level. The median sale price of an existing home rose 1.8% on the year in June, lagging the month’s 3.5% increase of average hourly earnings—housing affordability is gradually improving.

For a PDF version of this publication, click here: Comerica Economic Weekly, July 13, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.