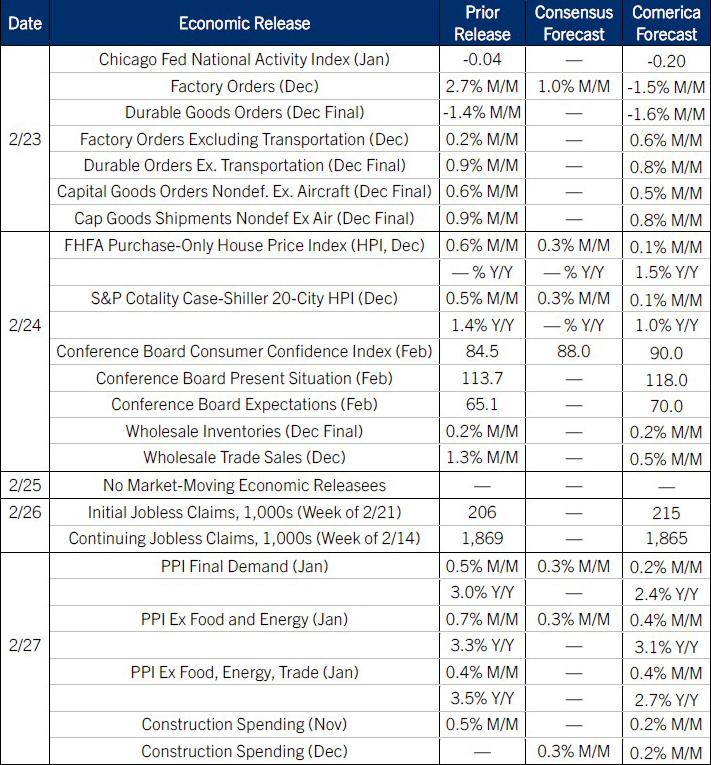

Preview of the Week Ahead

Benchmark house price indexes likely slowed at the end of 2025, closing the year with increases in the one-to-two percent range. Housing is still expensive, but affordability is improving as prices rise at a slower pace than incomes or household wealth. House prices will likely continue to rise at a modest pace in 2026. Their relative stability in recent years is making a helpful contribution to lower core inflation.

The Week in Review

Real GDP slowed to a 1.4% annualized increase in the fourth quarter of 2025, down from 4.4% annualized in the third quarter and undershooting the 2.8% consensus forecast. A drop in federal spending (Remember the government shutdown?) was a big headwind, subtracting 1.15 percentage points from annualized growth. Adjusted for that, the trend looked fine: Real final sales to private domestic purchasers grew a respectable 2.4% annualized—this measure of core GDP strips out swings in federal spending, inventory fluctuations, and the trade balance to track the trend. For 2025 as a whole, real GDP grew 2.2%, the slowest year since the 2020 recession. The slowdown is because the federal government tightened fiscal policy by cutting nondefense discretionary spending and raising taxes on imports (tariffs). This shrank the fiscal deficit to 5.8% of GDP—good!—but came at the cost of weaker growth—bad. Even so, 2.2% is fast enough real GDP growth for the U.S. The bigger issue is that job growth didn’t keep up with GDP, since employers added just 15,000 jobs per month last year.

In December, the personal consumption expenditures price index rose 0.4% on the month and 2.9% on the year. The core PCE price index also rose 0.4% on the month and was up 3.0% from a year earlier. Supercore PCE inflation—services prices excluding energy services and housing—was up 0.3% on the month and 3.3% on the year. 2025 marked the fifth consecutive year with inflation overshooting the Fed’s 2% target. The big drivers of price increases last year were rising electricity and heating bills and more expensive imported consumer products. Climate change added to inflation, too, raising the cost of homeowners insurance and beef prices (chronic drought has shrunk the U.S. cattle herd to the smallest in decades).

Personal income rose 0.3% in December while personal spending rose 0.4%. With spending rising faster than income, the personal saving rate edged down to 3.6% from 3.7% and reached the lowest level since October 2022. The depressed saving rate illustrates the strain on households from a softer job market and affordability pressures, helping explain why consumer surveys have been glum.

From the Fed’s perspective, the economy’s growth momentum looks fine, but inflation is still too high. The Fed can be expected to hold short-term rates steady until Chair Powell’s term ends in May. Economic growth will ride tailwinds in 2026 from lower taxes, more government spending, the Fed’s rate cuts last year, an improving housing market, the continuing AI boom, and refunds of the reciprocal tariffs that the Supreme Court invalidated February 20. The biggest downside risk to growth is from labor supply bottlenecks which could fuel a rebound of inflation.

For a PDF version of this publication, click here: Comerica Economic Weekly, February 23, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.