Preview of the Week Ahead

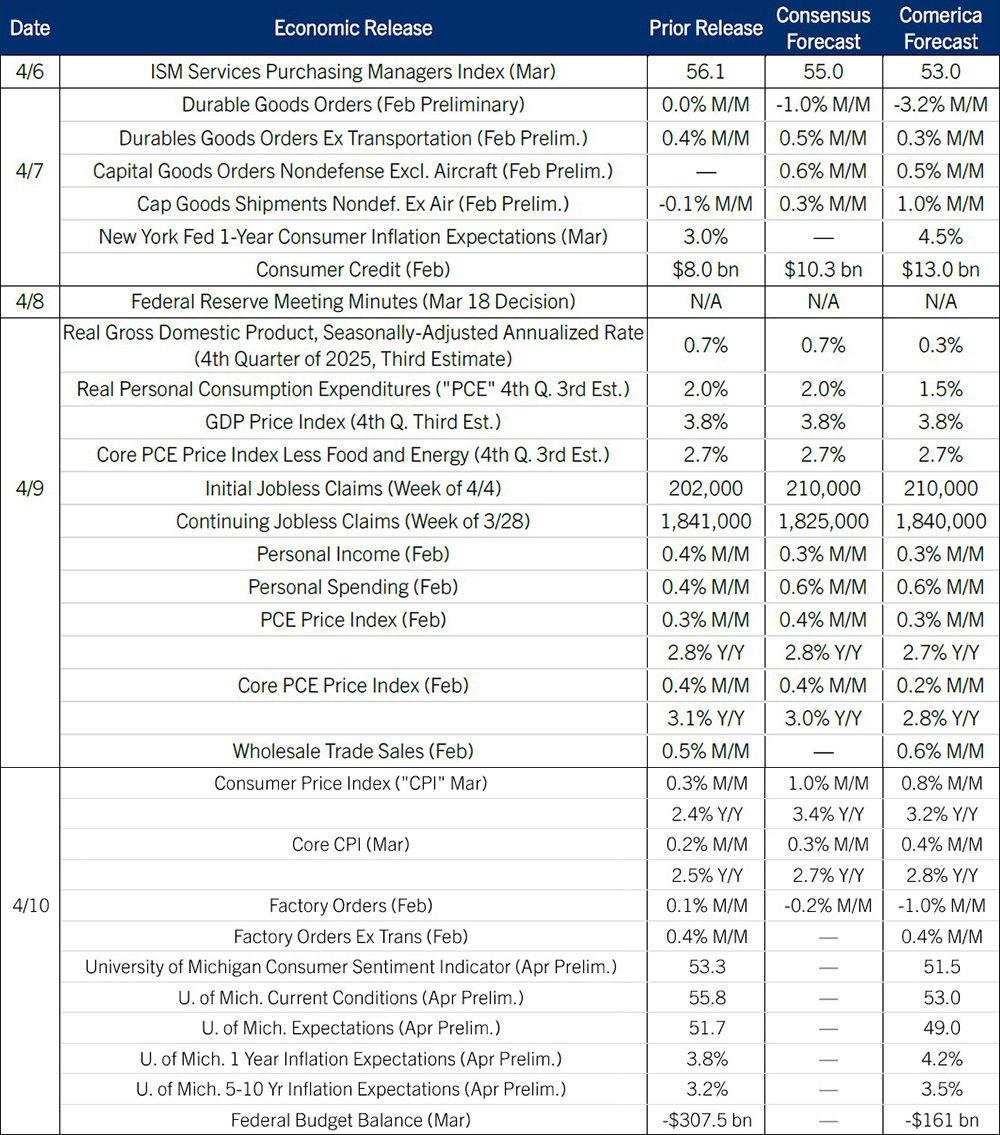

The CPI is forecast to climb back above 3% in the March release on surging prices of gasoline, which last week topped $4 per gallon for the first time since 2022. Core CPI also is expected to firm as airfares rise. Minutes from the Fed’s March 18 meeting will likely reinforce the message that interest rates are on hold until policymakers have a better understanding of how the Iran War is affecting the U.S. economy. Real GDP growth in the fourth quarter of 2025 will likely be revised lower, reflecting weaker consumer spending on services. The week also will bring the Fed’s preferred measure of inflation for February (PCE), thought it will matter less for financial markets than usual since the war subsequently pushed inflation higher in March.

The Week in Review

The March jobs report was considerably stronger than expected: Payrolls rebounded by 178,000, more than offsetting February’s 133,000 drop (revised from a 92,000 decline). With revisions, payrolls rose an average of 68,000 per month in the first quarter of 2026, well above the 10,000 monthly average in 2025. The unemployment rate edged down to 4.3%, but the details of the household survey were soft: Employment fell 64,000, unemployment fell 332,000, and the labor force shrank 396,000. The labor force participation rate dipped to 61.9% from 62.0% and was the lowest since 2021. Much of the decline reflects demographics. Prime-age (25-54) participation slipped to 83.8% from 83.9% in February but remained close to January's 84.0%, which tied for the highest since 2001. Wage growth cooled: Average hourly earnings rose 3.5% year-over-year, the slowest pace since 2021.

This is an on the one hand, on the other kind of a job market. Job growth is modest, but labor supply growth is limited, too. After March’s decline, the labor force hasn't grown since January 2025, as retirements rise and net inflows of foreign-born workers slow. Hiring is meager, but layoffs are low, too. This is a difficult job market for new grads, but it's a pretty good one for experienced workers—it stands repeating that the prime-age participation rate is near a multi-decade high.

This report’s reference period was the week of March 8 to March 14, far too early to show how the Iran War will affect the labor market. The war’s effect on global energy supplies could prove short-lived or prolonged, and could be modest or severe. Each path would imply a different outlook and policy response. With outcomes uncertain, the Fed can be expected to hold rates steady for at least the next few meetings while they assess incoming data and news about the conflict.

Retail sales jumped 0.6% in February after a revised 0.1% decline in January, as consumers returned to stores after January’s harsh weather. New car and light truck sales rose to a 16.34 million annualized rate in March from 15.75 million in February, which will boost the subsequent retail sales report, too. The trade deficit widened in February, and the White House adjusted tariff rates again after the report.

For a PDF version of this publication, click here: Comerica Economic Weekly, April 6, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.