Preview of the Week Ahead

The Fed is expected to hold rates steady this Wednesday at the final decision of Chair Jerome Powell’s term. The post-meeting press conference will probably focus on Powell’s future and legacy. Will he retire, now that the Justice Department has announced it is dropping the probe into his conduct as Chair? Powell said at the Fed’s March press conference that he has “no intention of leaving the Board until the investigation is well and truly over,” and Senator Thom Tillis blocked the confirmation of Powell’s successor until he is satisfied the probe is resolved. Powell’s term as governor runs on a separate timeline from his term as Chair and extends into early 2028, so he could continue serving as acting Chair until President Trump’s nominee Kevin Warsh is confirmed—or longer if he believes it is necessary to protect the Fed’s independence.

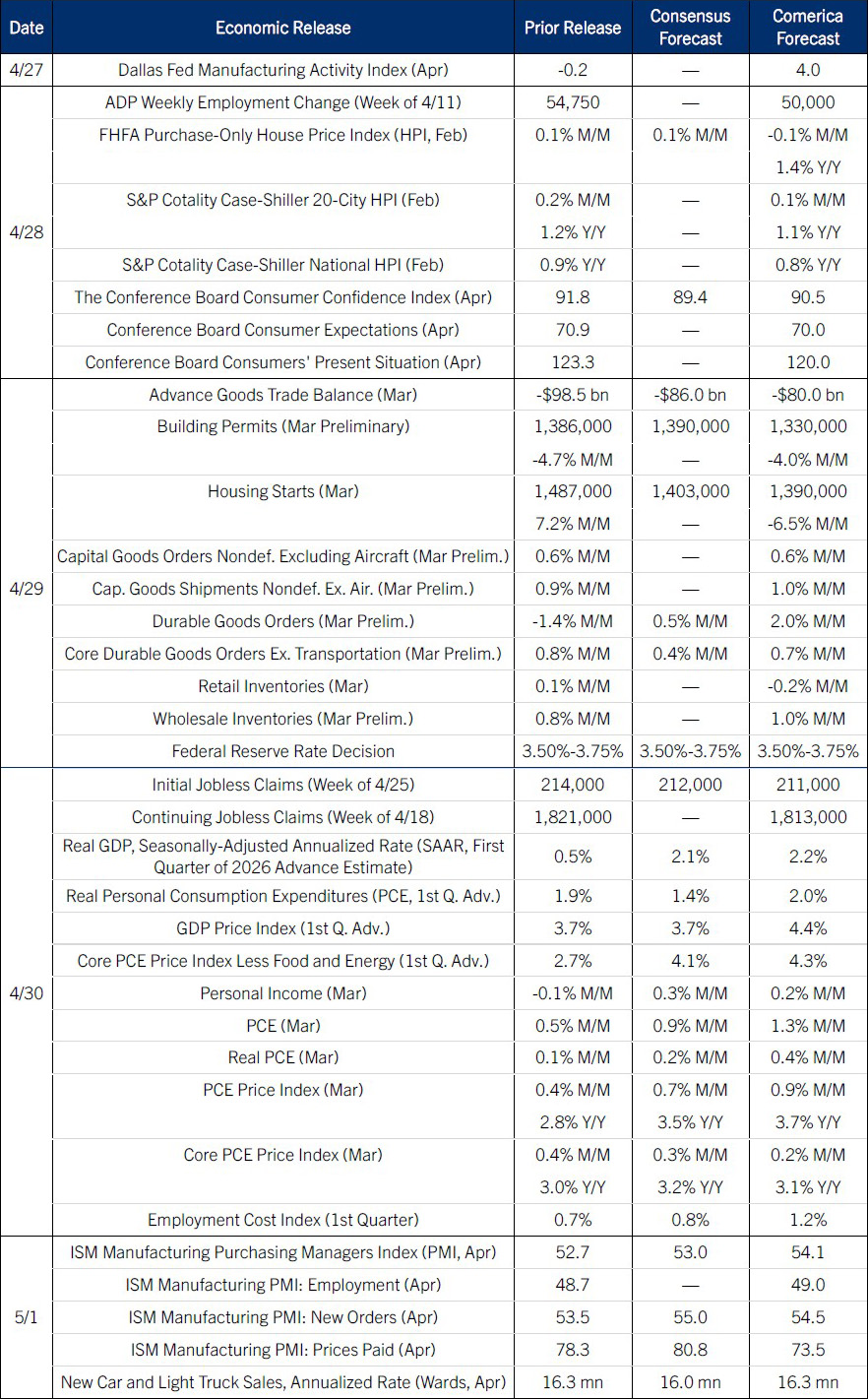

Real GDP likely rose moderately in the first quarter, supported by a big rebound in government spending after last year’s government shutdown ended. AI likely continued to fuel robust growth in fixed investment in computing equipment, software, and research and development in the quarter. Consumer spending growth was likely moderate as larger tax refunds offset the headwind from higher gas prices. The personal income and outlays report for the month of March, also due this week, will likely show headline PCE inflation drifting up toward 4% on higher energy prices, while core PCE inflation holds closer to 3%.

The Week in Review

Early April data suggest the economy is expanding at a solid pace despite anxiety over the Iran war. ADP’s weekly index of job growth accelerated to 55,000 per week in the April 4 release. Reported as a four-week rolling average, that pace is equivalent to a monthly increase of more than 200,000. The last time ADP reported job growth that strong was in mid-2024. Since ADP’s weekly index is relatively new, but it is worth watching given ADP’s standing as a leading source of private data on the U.S. economy. Markets will put more weight on the signal if the established monthly jobs reports from ADP and the Bureau of Labor Statistics (BLS) corroborate it. Other labor market indicators for early April are mostly encouraging: Initial and continued jobless claims held at low levels through mid-month, and job postings on Indeed.com have been roughly steady since the first quarter, a useful leading indicator for the BLS’s less timely job openings report.

In survey data, the U.S. purchasing managers indices (PMIs) published by S&P Global strengthened in the preliminary April releases. The manufacturing PMI rose to a four-year high of 54.0, while the services PMI returned to expansion at 51.3 after 49.8 in March. As expected, the surveys reported the largest increases in input costs since 2022 as the war pushed up petroleum prices and transportation costs.

The main exception to early April’s good news was consumer sentiment. The University of Michigan’s Consumer Sentiment Indicator was revised up to 49.8 in the April final release from 47.6 in the preliminary estimate but the month’s print remained an all-time low (Data go back to the late 1970s). The survey is designed to be more sensitive to cost-of-living concerns than other consumer surveys and is capturing consumers’ worries about gas prices and inflation more broadly. By comparison, Morning Consult Index of Consumer Sentiment also fell in April, but held above its lows in 2020 and 2022.

For a PDF version of this publication, click here: Comerica Economic Weekly, April 27, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.