Preview of the Week Ahead

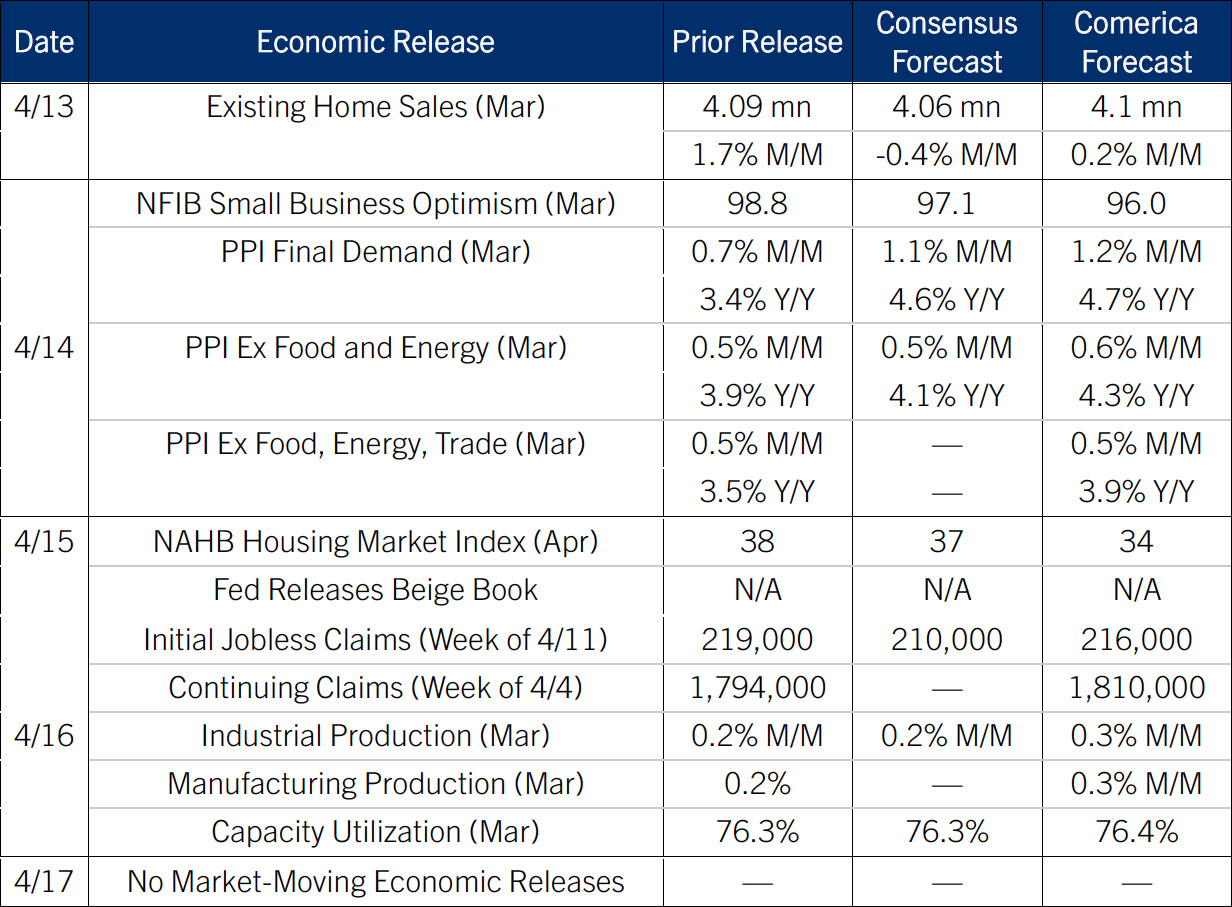

Echoing last week’s CPI release, producer prices rose sharply in March as the Iran war pushed up prices of crude and refined petroleum products and transportation charges. Producer price inflation was already outpacing CPI and PCE inflation before the war, and the gap is widening. This mostly reflects the larger weight of petroleum products and other commodities in the PPI compared to the consumer basket. Even so, the longer producer prices stay high, the more they will pull up consumer prices beyond those paid at the gas pump.

Existing home sales likely held about steady in March. The delay between when homebuyers choose a home, apply for a mortgage, and close means March’s sales tell us more about consumers’ mindsets in January and February than since the war broke out. Mortgage rates rose in March and April, another of the war’s knock-on effects, which will restrain home sales in April and May—more important months than March for the highly cyclical housing market. The median price of a home sold likely held about flat from a year earlier in March.

Industrial production is forecast to rise solidly in the March report on stronger manufacturing and mining output. Utilities production likely fell as the weather turned milder. U.S. crude oil production trended lower in March but will soon increase if high prices are sustained.

The Week in Review

Consumer sentiment fell to a record low this month on unhappiness over inflation and personal finances. The University of Michigan’s Sentiment indicator fell to 47.6 in the April preliminary release, below past cyclical lows like June 2022’s 50.0, November 2008’s 55.3, or May 1980’s 51.7. The survey was conducted almost entirely before the ceasefire on April 7, so the April final release in a few weeks should be stronger. The CPI jumped 0.9% in March on a 21% surge in gasoline, and was up 3.3% from a year earlier, the largest increase since May 2024. The core CPI was much better behaved, up just 0.2%, as lower prices of used cars and pharmaceuticals offset higher airfares. Businesses will take time to pass on increased energy costs to consumers. 2026 is shaping up to be the sixth year in a row with inflation overshooting the Fed’s 2% target.

The ISM Services PMI pulled back to 54.0 in March after jumping to 56.1 in February, the highest since 2022. March’s details were soft, with the employment component of the survey falling to the weakest since December 2023 and input prices rising at the fastest pace since 2022. Even so, the first quarter saw the headline index average the strongest level in three and a half years. Service-providing businesses had good momentum going into the shock of the Iran War, buoyed by tax cuts, increased government spending, and the interest rate cuts that the Fed made in the second half of 2025.

Real GDP in the fourth quarter of 2025 was revised down to 0.5% annualized in the third estimate from 0.7% in the second estimate and 1.4% in the first estimate. The government shutdown is the culprit behind the weak GDP print. Gross domestic income looked better, up 2.6% annualized in the fourth quarter. In year-over-year terms, real GDP grew 2.0% in the fourth quarter and real gross domestic income grew 2.4%.

For a PDF version of this publication, click here: Comerica Economic Weekly, April13, 2026

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.