Preview of the Week Ahead

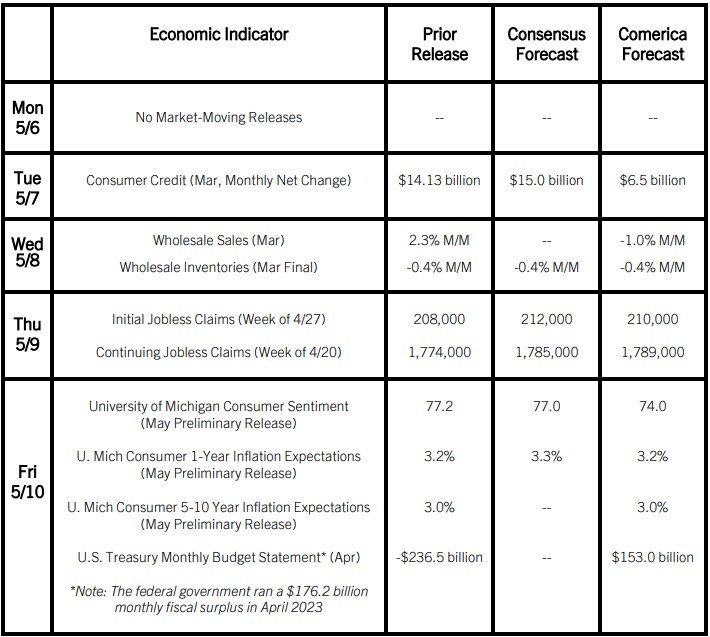

The U.S. Treasury Department’s Monthly Treasury Statement for April will be the most important release in a light week for economic data. Fiscal receipts usually jump in April as Americans submit payments for their annual income tax filings, which swings the fiscal balance to a surplus, even in years when the government runs an annual deficit. Capital gains tax receipts rose from April 2023, since the stock market did much better in 2023 than in 2022. But daily data indicate the government’s net debt fell less in April 2024 than in April 2023, suggesting expenditures may have risen even more than receipts compared to a year earlier.

Wholesale sales likely fell in March after a big increase in February, as crude oil production dipped and inventories on car dealer lots fell for a second consecutive month. Consumer credit likely rose more slowly in March than February.

The Week in Review

Matching Comerica’s forecast and the market consensus, the Federal Open Market Committee held the federal funds target unchanged at a range of 5.25% to 5.50% at the May 1 decision, and announced that they would slow the pace at which they run off their balance sheet to $60 billion per month in June from $95 billion previously. The Fed’s forward guidance emphasized that monetary policy is data dependent, meaning that the Fed would only begin to reduce interest rates after convincing evidence that inflation is slowing further. Comerica’s May forecast will project two quarter percentage point interest rate cuts by the Fed by year-end, at the September and December decisions.

Nonfarm employment rose a smaller-than-expected 175,000 in April, with 22,000 in net downward revisions to February and March. The unemployment rate edged up to 3.9% from 3.8% in February, with employment in the household survey 25,000 higher, unemployment up 63,000, and the size of the labor force up 87,000. The household survey is likely undercounting labor force growth since the statistical system has a hard time measuring economic activity of recent immigrants. Average hourly earnings increased 0.2% from February and 3.9% from a year earlier. The moderation of wage growth is a reassuring sign that the economy continues to move two steps forward, one step back toward more normal price pressures. In related data released at a lag, job openings, hires, and quits all pulled back in March to the lowest levels since the recovery from the pandemic took off in late 2020 and early 2021.

Other price data released last week were less encouraging than average hourly earnings. House prices rose more than expected in February, with the CoreLogic Case-Shiller S&P 20-City House Price Index up 0.6% on the month, well above the 0.1% consensus. The FHFA HPI overshot expectations even more and jumped 1.2%, versus a 0.2% consensus forecast. The ISM Manufacturing and Services PMI surveys both pointed to higher price pressures from input costs in April, with manufacturing input prices registering the most widespread increases since mid-2022. Both the Services and Manufacturing PMIs fell to below 50 in April, a sign private-sector economic activity lost momentum in the month.

For a PDF version of this publication, click here: Comerica Economic Weekly, May 6, 2024

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.