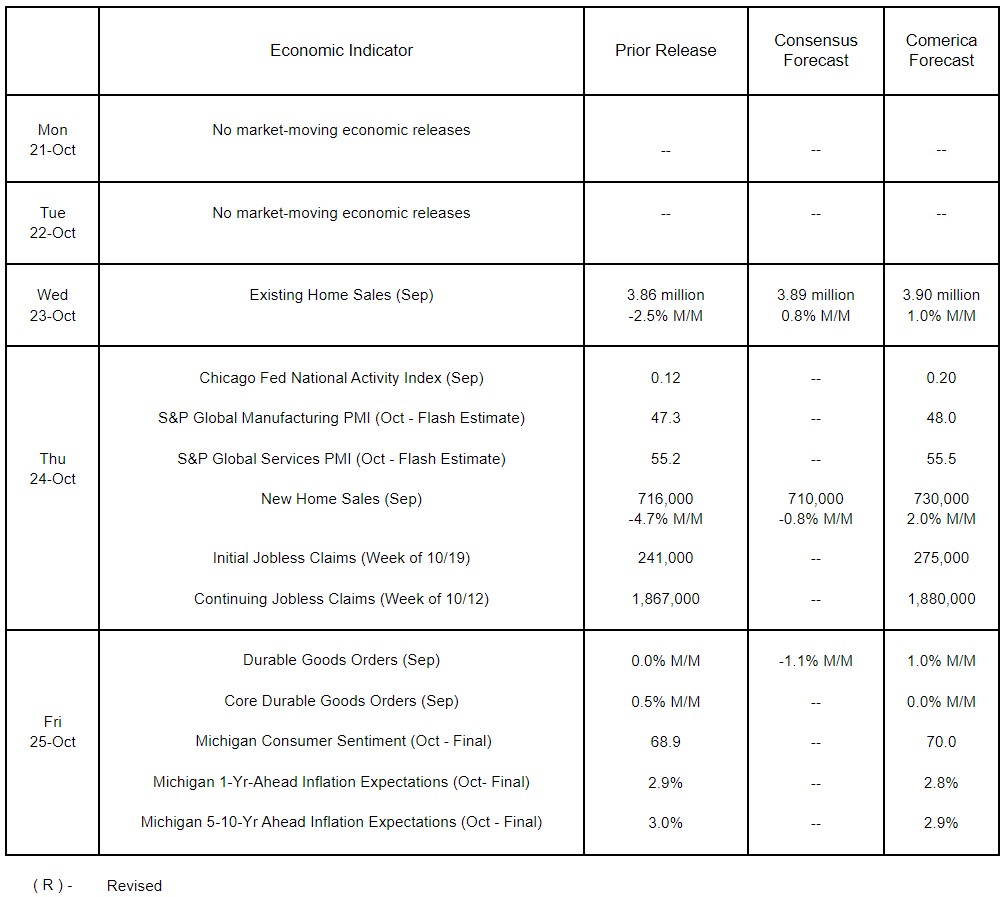

Preview of the Week Ahead

The economic calendar is relatively light again this week. Markets will get a first glimpse of business conditions in October, when S&P Global releases the preliminary (flash) estimates of its Manufacturing and Services Purchasing Managers’ Indices (PMI) on Thursday. Activity in the manufacturing sector is expected to have remained in contractionary territory, while the services sector likely expanded further. Durable goods orders are expected to have rebounded from a flat reading last month. Core durable goods orders, a widely-watched proxy for business spending on machinery and equipment, likely held steady. Existing and new home sales data are the other key releases this week. The consensus expects existing home sales, which account for most of the homes sold, to have rebounded in September after a steep fall in August. New home sales probably held steady. Markets are also likely to keep an eye on the University of Michigan’s final release of consumer sentiment for October. Sentiment probably rose higher, while households’ short-term and long-term inflation expectations likely held within the ranges observed over the past several months.

The Week in Review

Retail sales rose by 0.4% in September after modest growth in the prior month and exceeded the 0.3% consensus expectation. The gains were broad-based, with sales at 9 of the 13 retail subsectors up. Reflecting the sharp 4.1% decline in gasoline prices, sales receipts at gasoline stations tumbled by 1.6%. Core retail sales, used in the computation of nominal spending on most goods in the GDP report, rose by 0.7%, indicating a strong finish to the third quarter. Retail sales are likely to fall in October, as vast swathes of the southeast begin to recover from the devastation caused by hurricanes Helene and Milton.

Industrial production unexpectedly shrank by 0.3% in September. A 0.4% decline in manufacturing output led the overall contraction. Aerospace and miscellaneous transport equipment production cratered by 8.3%, reflecting the impact of the Boeing strike. Mining output also declined by a sizeable 0.6%, while utilities output increased by 0.7%. In line with lower industrial activity, capacity utilization fell further to 77.5% and was notably below its long-term average rate of 79.7%. At first glance, last months’ industrial production report is soft. However, the weakness, caused largely by the Boeing strike, should dissipate, as the labor dispute is resolved.

The National Association of Home Builders / Wells Fargo Housing Market Index improved slightly by 2 to 43 in October and was roughly in line with the consensus. There was a notable divergence between subindices gauging current conditions and future expectations. The present sales and buyer traffic subindices, which measure the current state of the new home market, both rose modestly but held well below their historical averages. The rebound of mortgage rates in recent weeks likely soured homebuilder sentiment. The future sales subindex, on the other hand, rose solidly and was roughly in line with its historical average. Homebuilders remain downbeat in their assessments of the current state of the housing market, but see brighter prospects in the coming months.

For a PDF version of this publication, click here: Comerica Economic Weekly, October 21, 2024

The articles and opinions in this publication are for general information only, are subject to change without notice, and are not intended to provide specific investment, legal, accounting, tax or other advice or recommendations. The information and/or views contained herein reflect the thoughts and opinions of the noted authors only, and such information and/or views do not necessarily reflect the thoughts and opinions of Comerica or its management team. This publication is being provided without any warranty whatsoever. Any opinion referenced in this publication may not come to pass. We are not offering or soliciting any transaction based on this information. You should consult your attorney, accountant or tax or financial advisor with regard to your situation before taking any action that may have legal, tax or financial consequences. Although the information in this publication has been obtained from sources we believe to be reliable, neither the authors nor Comerica guarantee its timeliness or accuracy, and such information may be incomplete or condensed. Neither the authors nor Comerica shall be liable for any typographical errors or incorrect data obtained from reliable sources or factual information.